This is Part 1 of a two-parter, about how the housing crisis causes debt-bondage and wage-slavery, and how the housing Commons can release people from debt and give them freedom to do what they know needs to be done.

In Stroud Commons, we’re looking to find ways to speed up the building of the commons – especially the housing commons, which we were talking about in terms of ‘the rock on which the commons can be built’ before we’d even formed the core group in Stroud. Dil Green of Mutual Credit Services (MCS – who design models for the commons in all sectors), posted a message in our chat group, giving his take on the housing crisis, and how we might speed up the housing commons by allowing / helping / encouraging people to put their house into the commons, and carry on living in it for the rest of their life – and pass it on to their family, too. They’d be able to free up cash (like equity release, but without having to go into more debt), they could retire early, maintenance of the property would be taken out of their hands, and as they get older, commoners will visit regularly to chat, check they’re OK and see if they need anything. Freed from debt-bondage and wage-slavery, and with greater security, people will have more time. And they would spend it on things they know need to be done.

We’ve turned the thread into a 2-part article. Part 1 is about the housing crisis, and Part 2 is about how the housing commons can help solve it.

First, let’s look at the problem:

How the housing crisis causes debt-bondage and wage-slavery

There is a housing crisis in the UK, but it’s not the way the papers frame it – which is all about numbers of houses, nimbys, building on the green belt or building council houses – it’s not a supply problem, really – it’s a distribution problem, caused by over-inflated prices.

The reason we’re told it’s a supply problem is because there is so much money (and employment) in housing development, and because the UK finance system is hooked on mortgage income. All politicians (even the Greens) seem gung-ho on building more houses. But house building is an enormous cause of CO2 emissions and other environmental degradation. Surely, we should be looking to solve the distribution problem – dealing with house prices – before digging up the green belt?

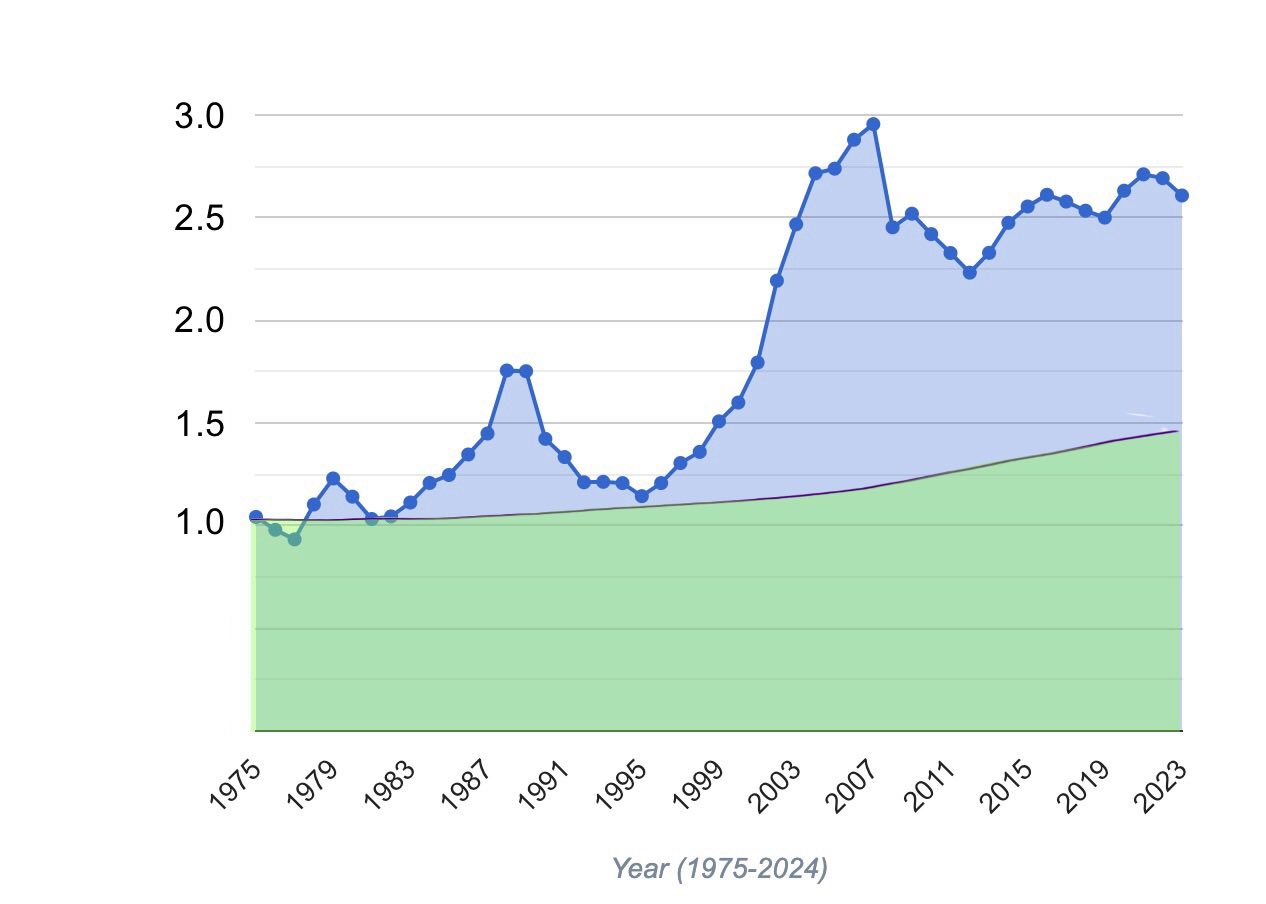

The graph shows UK house price inflation in blue and population growth in green; clearly, this is not a simple supply/demand relationship. It is best described as a government sponsored ‘Ponzi scheme’ – where the ‘too good to be true’ rewards are paid for by ‘greater fools’ joining in – until the whole thing crashes. Similar schemes are under way in every country across ‘the West’.

Over the last fifty years, the cost of having a secure place to live has eaten up a larger and larger fraction of people’s income. Over the period of the graph, the price of UK housing has approximately doubled in relation to earnings.

This has gone hand-in-glove with the campaign to turn more and more people into ‘home-owners’ – aka slaves to mortgage debt for most of their working lives.

Employers are told – ‘if you want a reliable worker, look for someone with a mortgage and 2 kids’. Why? Because they will undergo almost any pain in order to provide a safe place for those kids to live, and they are already in debt-bondage. Wage-slavery comes as part of the package.

The ‘reward’ for participation in this programme has been the enrichment of a small fraction of the population – those lucky enough to get onto the ‘ladder’ early on (ie at least 20 years ago). The problem with this is that the upwards escalator of house prices cannot carry on forever – there is only so much of your income that can be allocated to a place to live, and it’s already too high for most. Those rewards are simply not possible for most people under the age of 40.

The 2008 crisis was triggered by the housing market in the US, and that instability is not going away – there will be other crises, and soon. In the UK, the ‘value’ of the housing stock is now considered to be somewhere between £7-8 trillion – around £200,000 per working person (about half of us). Since we all buy our houses on debt, and mortgages double the initial price of the houses we (and landlords) buy, that suggests that every working person will spend £400k on having somewhere to live in their lifetime – but the average lifetime income is only £570k! Something has to break.

The Housing Commons offers a way out of this mess, a way which diminishes debt-bondage and wage slavery, de-risks the housing finance system, and does not attack individuals who ‘got lucky’ (after all, their lives have already been spent in wage-slavery and debt-bondage).

But there’s more. If we can, even by a fraction, free people from debt-bondage and wage-slavery, it will liberate them to do what, deep down, they know they want to do – work to secure their and their children’s longer-term future.

This is Part 2 of a two-parter, about how the housing crisis causes debt-bondage and wage-slavery, and how the housing Commons can release people from debt and give them freedom to do what they know needs to be done.

Let’s look now at the Housing Commons:

How the housing commons can solve the housing crisis

In Stroud, there’s a larger than usual fraction of the population that a) understands the mess we’re in, and b) is prepared to do something about it. As usual, though, we are significantly constrained in what we can do by access to resources. The first, most critical resource in these efforts is human life hours – we’re all stretching what we can achieve on that front.

Why? Because the system we live in acts to use up the life hours of humans in efforts to achieve safe housing, care for their nearest and dearest, and securing the basic necessities of life. It achieves this trick by enforcing the money system on us. The claims we have on others – in order to secure the basics, and the methods we use to confirm our own willingness to help secure the basics for others – have all been abstracted away from real life, into the money system.

We cannot easily build a life for ourselves that is significantly outside the existing money system (at least, not one which does not condemn us to disconnection from friends and family and community). It encroaches everywhere, at an increasing pace. Worse, that money system is, very obviously, degrading the biosphere – the foundation of all life. The money system has us locked down into short-termism, while it violently degrades our long-term prospects.

So far, so gloomy, and not news – although perhaps this analysis does a couple of things which seem useful to me. First, there are no ‘baddies’ in it (there are baddies in the world of course, but they’re no longer the issue – only an aspect); and second, there’s no ‘culture’ in the analysis – nothing about ‘dualistic worldview’. Again that perspective is not ‘wrong’, it’s just, in my view, a symptom, not a cause. A post rationalisation that helped lock us in.

So, what’s the point of this analysis? It’s a story to set up an argument for action. I happen to think it’s a well-grounded story, which is robust from many angles, but in the end it’s a story.

What’s the argument for action? Of course, it’s ‘Build Commons’. But I want to think about the ‘how’. How can we do such a mammoth job, when we’re so constrained? How do we find the time?

In a sane system, the question, ‘how do we find the time to save the world?’ would make no sense. If the world is at stake, you drop other things, because they’re irrelevant if the world is lost. The analysis shows us, though, how we’re trapped. How we’re forced, instead, to ask the question, ‘How do we find the money?’ Human time has been captured by money.

Happily, though, the mechanism of the trap offers a way out. Because the mechanism is debt: ‘I owe, I owe, it’s off to work I go’. And the biggest debt, the tightest trap, is mortgage debt. The property system. In order to have a safe place to live, to be, we are forced into debt bondage. Remember, the ‘mort’ in ‘mortgage’ means ‘death’. When you take out a mortgage, you stake your life on it. And boy does it eat your life.

If we aren’t yet in debt bondage, we must become time slaves – wage slaves – in order to achieve debt bondage – to ‘get on the housing ladder’, in the search for a secure place to live. They won’t even let you stake your life, unless you show willing, by becoming a slave (you get paid in arrears, of course, not up front, so you start your working life in debt).

What this means, and again with reference to Stroud, is that many people have built up a significant asset, through time/wage slavery (working). However, the asset is locked-down – really part of the finance system, not really yours. Your house may be worth a lot of money on paper, but you can’t have that money without either selling your house or going back into debt bondage (remortgage). And you can only sell it to someone who can get a mortgage – guaranteeing another doubling for the finance system. So what to do?

There is no possible ‘ great awakening’ and no effective one either. That’s not the route. That’s the ‘fault in our culture’ thinking trap.

I don’t think people are asleep. I think they’re trapped, and have no obvious agency – either as individuals, or as community, to achieve anything that seems likely to build something better, for the simple reason that (intuitively rather than rationally) they understand that if they challenge the money system, their children suffer, and their old age looks bleak. So they do what life does in times of trouble, and reduce the time horizon they worry about. They do what works now and cross their fingers about a future they don’t feel they can influence.

What they need – and perhaps this would be a kind of awakening – is evidence of agency from working together. Agency that builds security and reduces future risk. And again, that is Commons. But they need working examples, not words or stories. We’re building in Stroud. But it’s slow – mainly because of constraints on our time and the money to engage the time of others with.

And here’s the way through. We need to build the Housing Commons model, in particular, to arrive at the point where we can see that putting our own houses in makes sense. This will liberate us from time slavery and liberate lots of cash too.

But please don’t think that this is either a moral call, or one for collectivisation! I’m emphatically not saying ‘put your family on the line to save the world’. What I am saying is that we need to concentrate on the Housing Commons model, on getting it to viability, on reaching the point where it looks like the obvious and safe thing to do to opt your house in, for tens, hundreds, thousands of people.

Because it will both liberate us from time/wage slavery and give us better security. And it will drive change like nothing else you will ever see. The UK housing market is driven by individual families making tough choices. We need only offer them better choices. The model works financially; all we have to do is make it work experientially. And the great thing is that we get to liberate ourselves early on – both those of us lucky enough to already own, and those of us in precarity.

The world in a decade from now will be shockingly different (as well as apparently the same). It’s building Commons that matters for security. And rent vouchers bring cash out of pension funds, which build the system, and into our hands, to build more Commons. That’s the point.

The more Commons we build, the safer we are, and the more of our basics are in our control, and the less debt we have, and the more time we have to heal the world, as best we can.

No other Commoning activity currently has the same power to do this as the Housing Commons, which is why it must be pushed hardest. Which is the greatest precarity people experience? Where is the debt-bondage? Which is the thing which drives people into wage-slavery? Where is all the product of their work locked away? It’s all housing. Forty years ago the answer would have been different. Weirdly, Margaret Thatcher built the conditions we can exploit.

The Housing Commons is like Aikido; it uses the force of the attack – the insane and dangerous cruelty of ever-increasing house prices – to provide the force whereby we preserve ourselves

— Dil Green, Mutual Credit Services.

Ed. note: Here’s the link to the original post on lowimpact.org.

And you?

In Stroud Commons, we’re looking to find ways to speed up the building of the commons – especially the housing commons, which we were talking about in terms of ‘the rock on which the commons can be built’ before we’d even formed the core group in Stroud. Dil Green of Mutual Credit Services (who design models for the commons in all sectors), posted a message in our chat group, giving his take on the housing crisis, and how we might speed up the housing commons by allowing / helping / encouraging people to put their house into the commons, and carry on living in it for the rest of their life – and pass it on to their family, too. They’d be able to free up cash (like equity release, but without having to go into more debt), they could retire early, maintenance of the property would be taken out of their hands, and as they get older, commoners will visit regularly to chat, check they’re OK and see if they need anything. Freed from debt-bondage and wage-slavery, and with greater security, people will have more time. And they would spend it on things they know need to be done.

Putting their home into the commons, and continuing to live in it could be very attractive to people as they get older. Dil said that he wasn’t sure how many people would go for it, but within 10 minutes, a couple of people in the group said they might – so it could be a winner.

- Here’s more info about the housing commons.

- Here’s more on rent vouchers (aka ‘use-credit obligations’).

- Here’s the latest on Stroud Housing Commons.

- Contact us if you’d like to get involved.