Last week, I gave a fairly wide-ranging presentation at the 2016 Biophysical Economics Conference called Complexity: The Connection Between Fossil Fuel EROI, Human Energy EROI, and Debt (pdf). In this post, I discuss the portion of the talk that explains several key issues:

- Why we are right now seeing so many problems with respect to wealth disparity and low commodity prices (Answer: World per capita energy consumption is already falling, and the energy/economy system needs to reflect this problem somehow.)

- Why the quest for growing technology leads to growing wealth disparity (Answer: The economy must be configured in more of a hierarchical pattern to support growing “complexity.” Growing complexity is the precursor to growing technology.)

- Why rising debt is an integral part of the energy/economy system (Answer: We could not pay workers for making long-lasting goods and services without using debt to “pull forward” the hoped-for benefit of these goods and services to the present, using debt and other equivalent approaches.)

- Why commodity prices can suddenly fall below the cost of production for a wide range of products (Answer: Prices of commodities depend to a significant extent on debt levels. A major problem is that when commodity prices rise, wages do not rise in a corresponding manner. Rising debt levels can mask the growing lack of affordability for a while, but eventually, debt levels cannot be raised sufficiently, and commodity prices fall too low.)

- The Brexit vote may be related to falling energy per capita in the UK. Given that this problem occurs in many countries, it may be increasingly difficult to keep the Eurozone and other similar international organizations together.

- My talk also touches on the topic of why a steady state economy is not possible, unless we can live like chimpanzees.

My analysis has as its premise that the economy behaves like other physical systems. It needs energy–and, in fact, growing energy–to operate. If the system does not get the energy it needs, it “rebalances” in a way that may not be to our liking. See my article, “The Physics of Energy and the Economy.”

An outline of my talk is shown as Slide 2, below. I will omit the EROI and Hubbert model portions of the presentation.

Slide 2

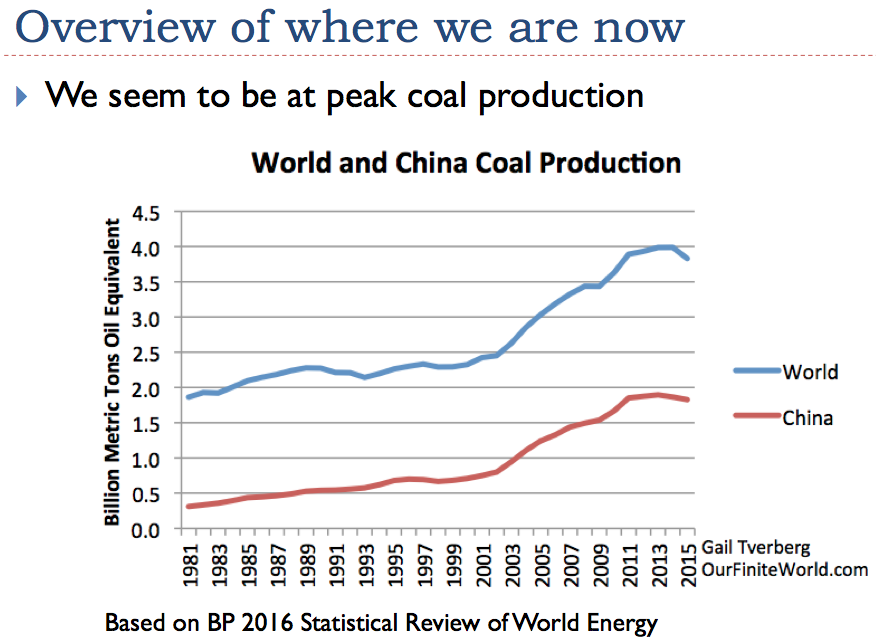

Peak World Coal Seems To Be Happening, Right Now

In the view of most of the researchers I was talking to at this conference, oil is likely to be the first problem, not coal. And the issue is likely to be high prices, not low. So peak coal now, as shown in Slide 3, doesn’t seem to make sense. Yet, my analysis of recent data strongly suggests that peak coal is exactly what is happening, right now.

Slide 3. World and China appear to be reaching peak coal.

I will show later in this presentation why peaking coal production does seem to make sense–price levels of all fossil fuels seem to vary together. The extent to which debt levels are growing seems to be a major factor in price levels. When the debt level is not growing rapidly enough, “demand” is not high enough, and prices for all fossil fuels tend to fall simultaneously. A related issue is the extent to which the world economy is growing; if world economic growth is too slow, this will also tend to hold down demand, and thus energy prices.

China’s rate of growth in coal production started falling back in 2012, which is when coal prices started falling. This is before China’s new leadership took over in March 2013. We know that coal production in China is likely to continue falling, because China’s energy bureau is reporting that China plans to close over 1000 coal mines in 2016, because of a “price-sapping supply glut.” See my article, “China: Is peak coal part of its problem?” for additional information.

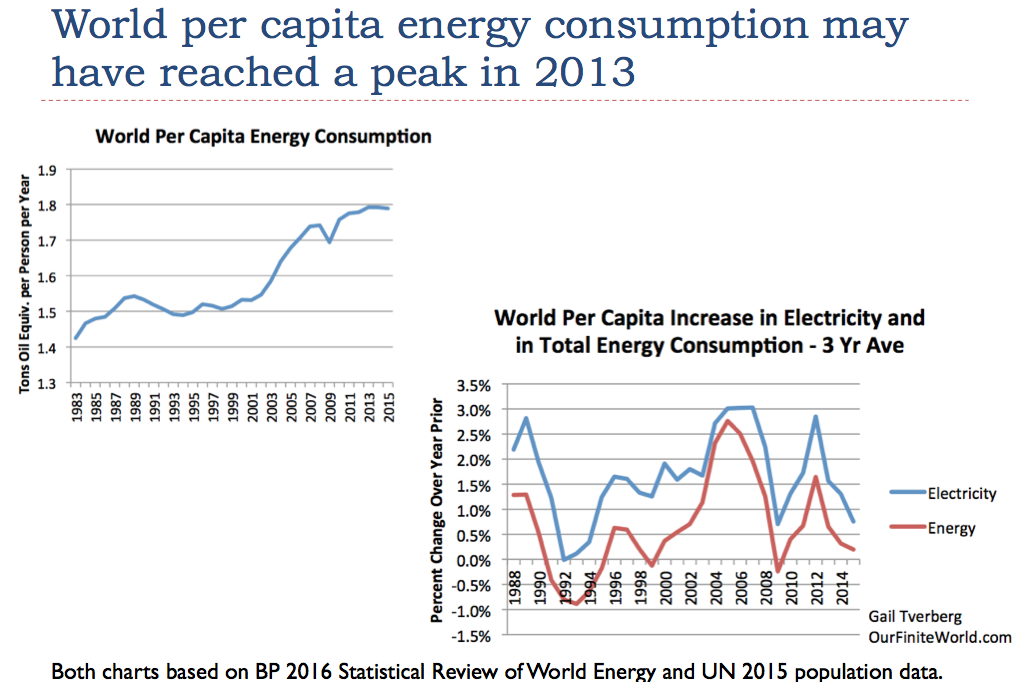

World Per Capita Energy Consumption Seems To Have Already Started Falling

Slide 4. World per capita energy consumption may have reached a peak

The reason why I say that world per capita energy consumption may have reached a peak in 2013 is partly because coal consumption appears to have peaked. If coal has peaked, it will be hard to make up the shortfall using other fuels, such as renewables, or even natural gas. Furthermore, recent world figures (shown above) already show a small drop in per capita energy consumption. If world coal production continues to drop, we can expect world per capita energy consumption to continue to drop.

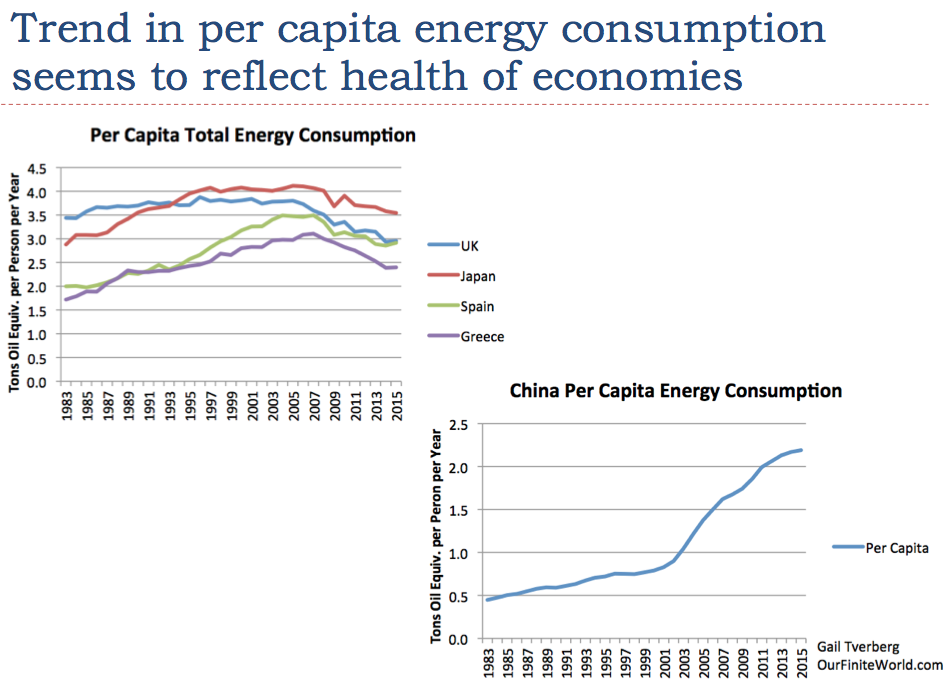

Energy Consumption Trends for a Few Countries

The figure below is not actually in the presentation–I thought I would add it now, to show energy consumption varies for a few economies. The upper chart in the Supplemental Slide shows the trend in per capita energy consumption in UK, Japan, Spain, and Greece. We know that Japan, Spain, and Greece have been experiencing economic problems for several years, something that perhaps should not be too surprising, given their falling energy consumption per capita. The UK shows a similar pattern to these three countries. Such a pattern is likely to lead to rising wage disparities, for reasons we will discuss later in this presentation, when we talk about “complexity.”

Supplemental slide. Per capita energy consumption trends for four advanced economies and for China, based on BP 2016 Statistical Review of World Energy and 2015 UN population data.

China’s energy consumption shows a contrasting pattern. China experienced rapid growth in energy consumption after it joined the World Trade Organization in 2001. Recently, China’s growth in energy consumption has been slowing, suggesting slowing growth in the economy–perhaps even more than reported in official GDP reports.

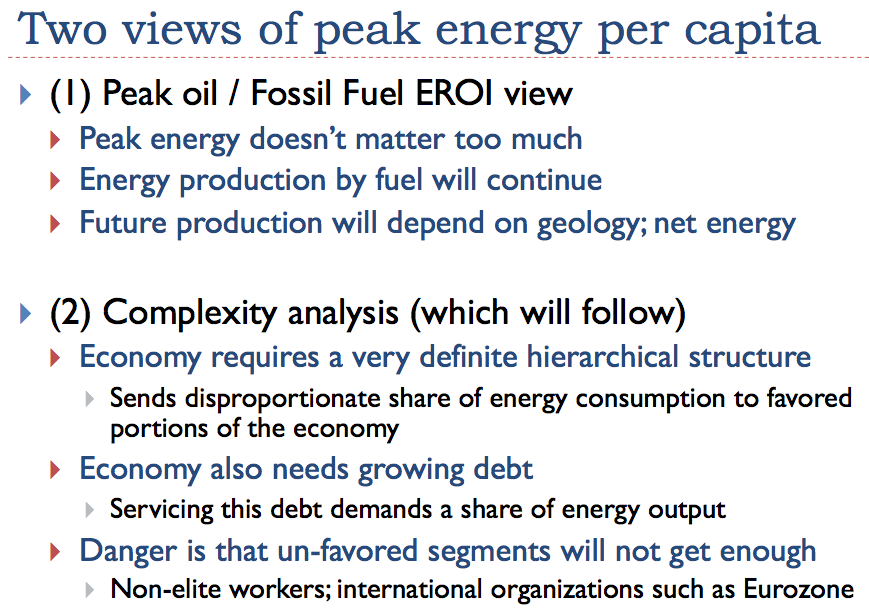

Why Peak Per Capita Energy Matters

In Slide 5, I give an overview of why peak energy per capita matters. My view is the second one shown on this slide. It is not that every segment of the economy will necessarily have problems. Instead, un-favored segments are likely to be first to have problems. Most conference attendees came with the first view.

Slide 5. Two views of peak energy per capita.

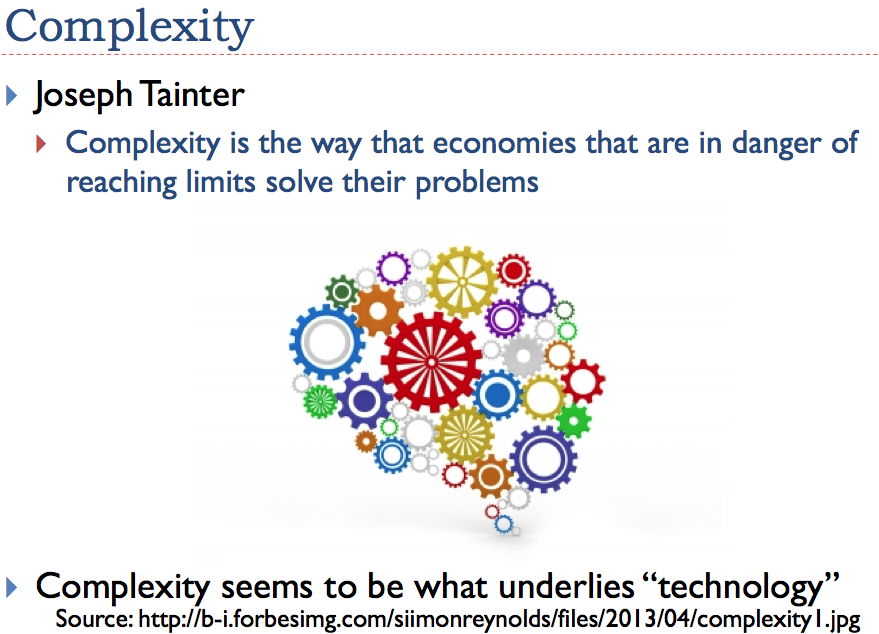

How the Economy Is Affected by Growing Complexity

Joseph Tainter in the Collapse of Complex Societies tells us that the way economies that are in danger of reaching limits can sometimes solve their problems is through increased complexity.

Slide 6. Complexity introduction

Economists today seem to believe that technology will solve our problems. I see complexity and technology as being related, with complexity being a precursor to technology. Economies that hope to adopt higher levels of technology need to take steps in the direction of growing complexity, to achieve this goal.

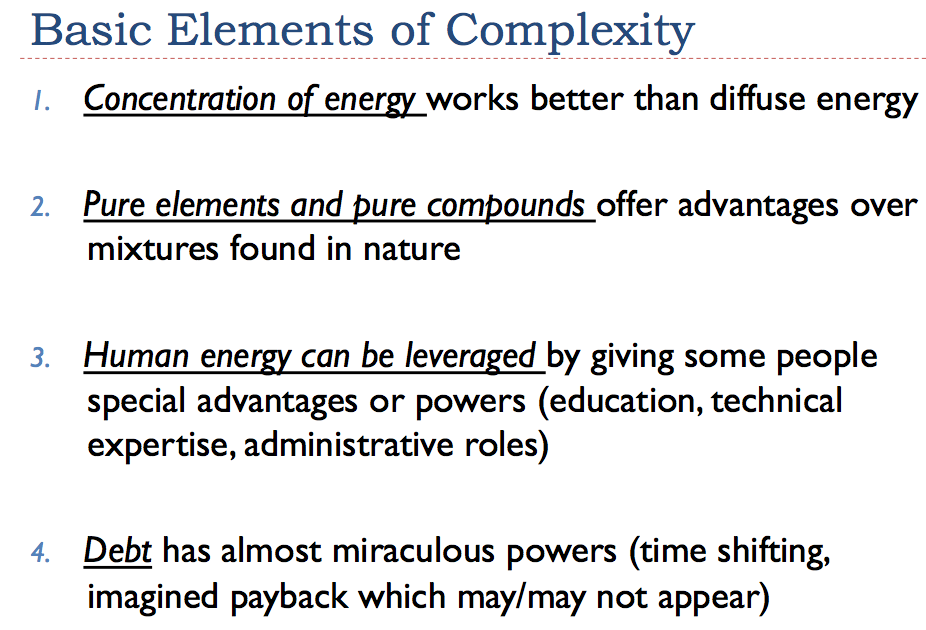

When I thought about what makes up complexity, this is the list of elements I came up with:

Slide 7. Basic Elements of Complexity

Regarding concentration of energy, the use of concentrated energy seems to be what sets humans apart from other animals.

Slide 8. Early use of concentration of energy

If we want a steady-state economy, “all” we need to do is set aside our use of concentrated energy, and live like chimpanzees. I am not sure how we keep our bigger brains adequately nourished. A couple of slides related to this are Slides 9 and 10.

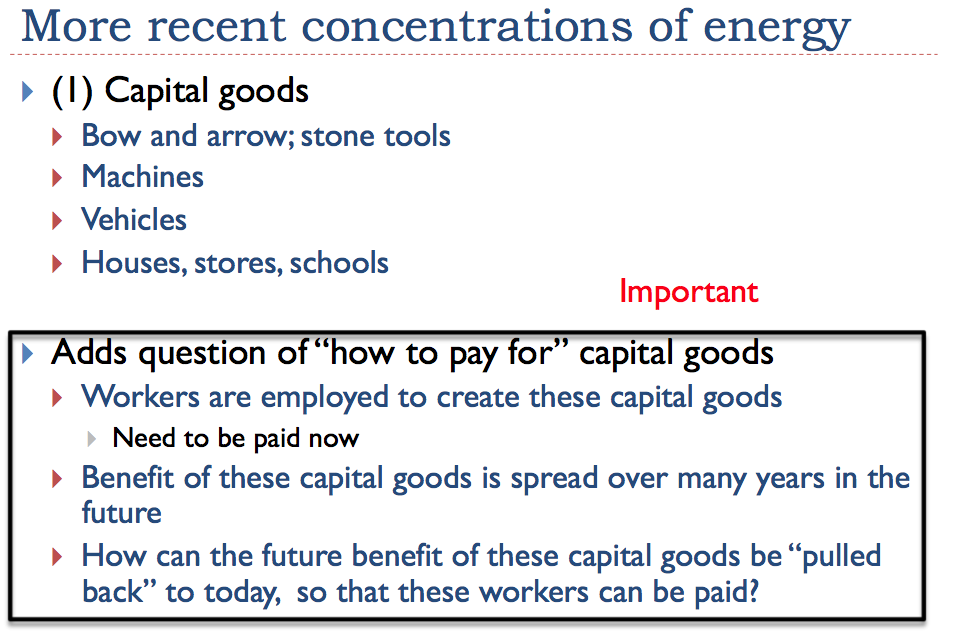

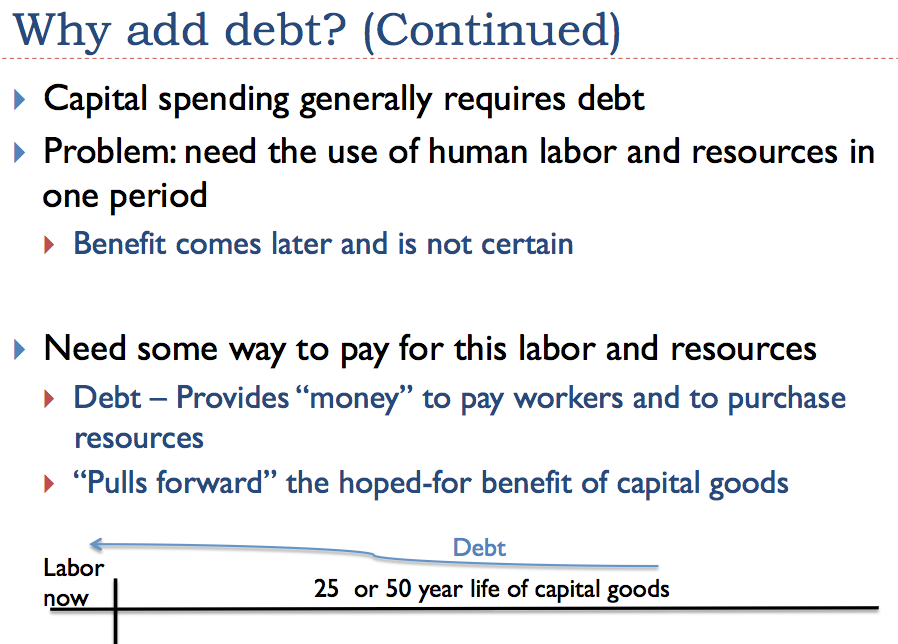

Another type of concentration of energy is capital goods. Capital goods are all of the goods that we expect to last for a fairly long time–things like homes, vehicles, and factories. The big issue is how to pay for capital goods.

Slide 11. Capital goods– more recent examples of concentrations of energy

The problem is that we need to pay workers now, but the benefit of these capital goods is spread over many years in the future. Somehow, the future benefit of these capital goods must be “pulled back” to today. The obvious answer to this predicament is the use of debt (or debt-like instruments) to fund capital goods. We will get back to the issue of debt later.

The next few slides (12 to 14) show other ways that concentrations of energy can be developed. One way is through the creation of businesses. Even larger concentrations of energy can be formed by creating bigger businesses, including international businesses. Governments can also be used to concentrate the use of energy resources, because of government’s ability to build roads, schools, and many other projects. International organizations can also act to concentrate wealth, by easing trade among members (Eurozone and World Trade Organization) and by lending money to member countries (International Monetary Fund and World Bank). All of these organizations can benefit from the use of debt to fund their growing organizations.

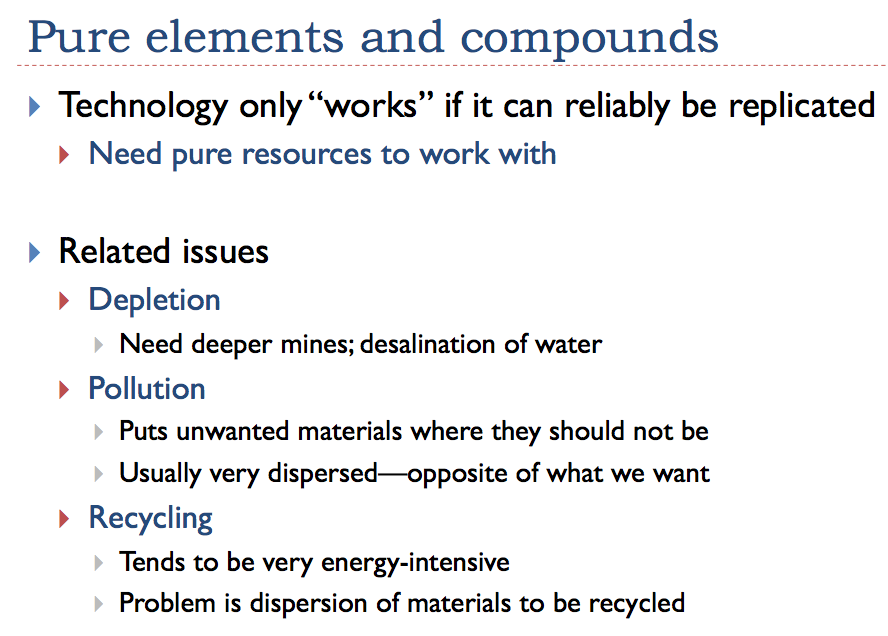

We said that concentration of energy was the first element of complexity (see outline at top). The second element of complexity is pure elements and compounds. In many ways, this requirement is similar to concentrations of energy, in the way it allows technology to work.

Slide 15. Why pure elements and compounds are needed for complexity

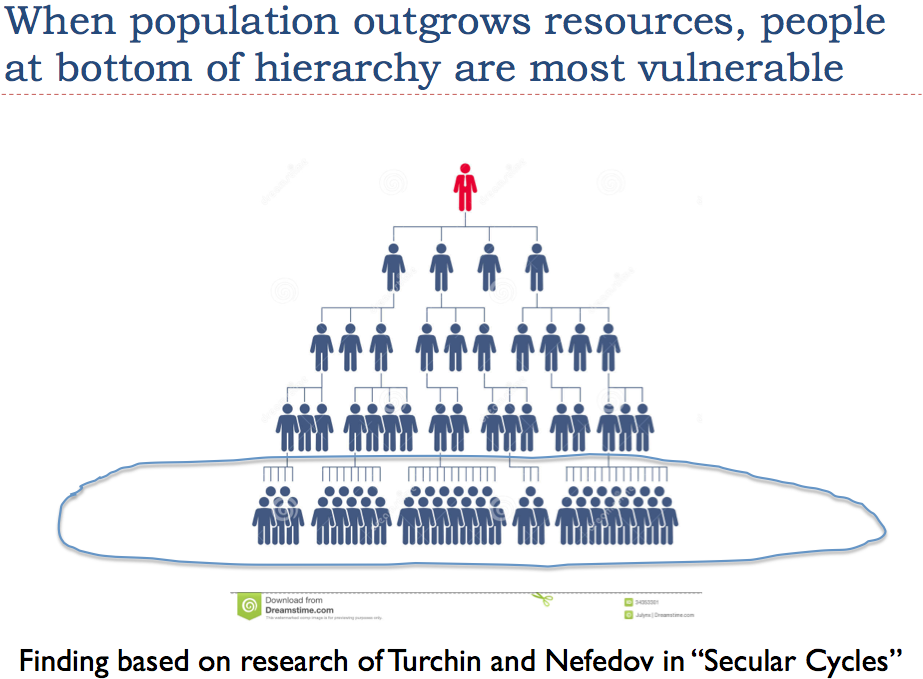

The third element of complexity (see outline at top) is leveraging of human energy through hierarchical organization. In many ways, this is the idea of concentrated energy, as applied to humans.

16. Leveraging of human energy through hierarchical organization.

Historically, the big problem has been populations that grew too large for their resource bases. In a way, we are reaching a similar predicament. Not too surprisingly, when this happens, it is the people at the bottom of the hierarchy who tend not to receive enough.

Slide 17. People at the bottom of a hierarchy are most vulnerable.

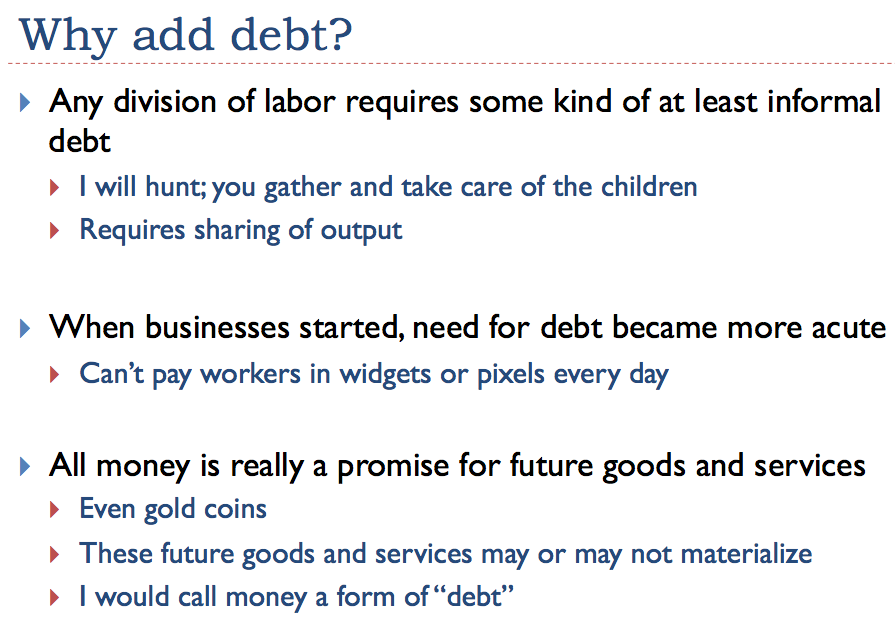

Why Debt Is Required

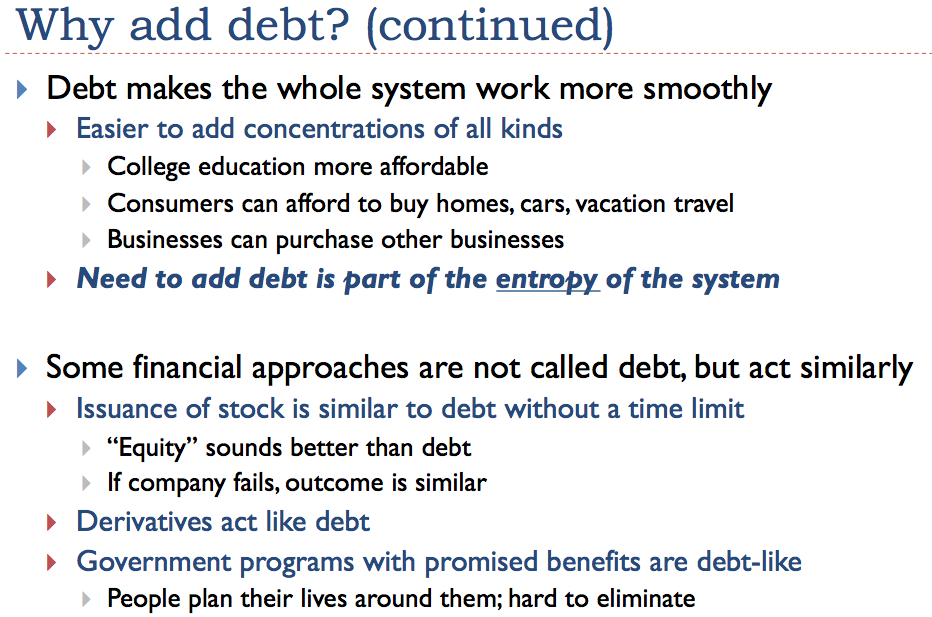

Slide 18 – Why add debt?

One of the fundamental benefits of debt is time shifting.

Slide 19. How debt allows time shifting.

Of course, the value of these capital goods is speculative, when debt is used to price them in advance. As long as capital goods, and other uses of debt, provide sufficient benefits to the economy so that debt can be repaid with interest, the system tends to work as planned.

Slide 20. Debt makes the economic system work more smoothly.

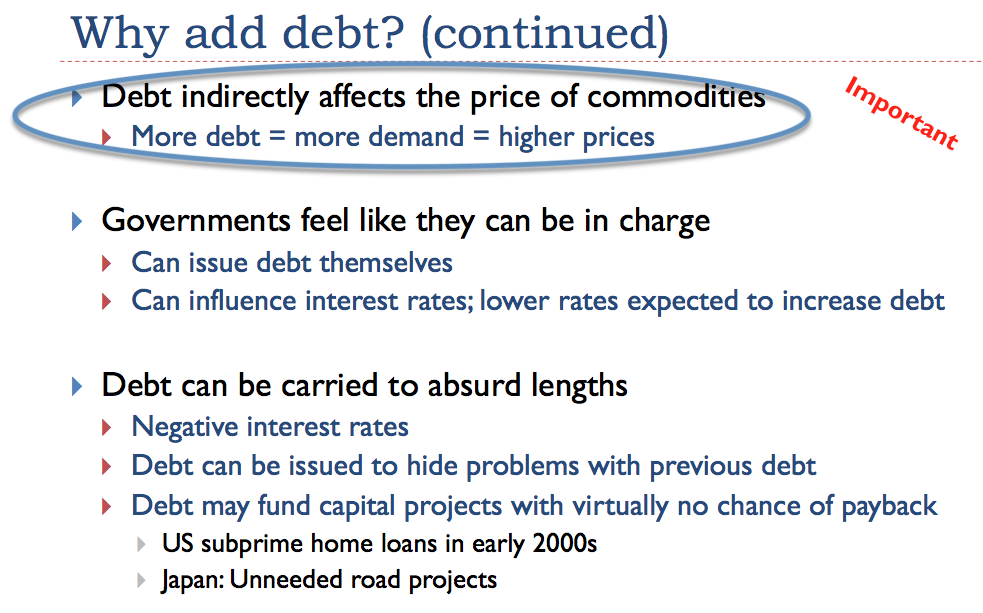

One key aspect of debt is its ability to determine demand, and thus prices, of commodities such as oil and natural gas. The reason why debt has almost magical power is because if a potential buyer is given a loan for any kind of capital good, say a house, or car, or factory, the potential buyer can purchase the capital good far sooner than if he or she needed to save up for it. Each of these capital goods requires commodities of various kinds, such as steel, copper, oil, coal, and natural gas. Thus, we would expect rising debt levels to raise the prices of a broad range of commodity prices, simultaneously.

21. Debt helps determine prices of commodities

We can think of the situation as follows: An economy that keeps growing is (in energy terms) an out-of-balance system. Rising debt levels help maintain this out-of-balance condition by providing ever-higher commodity prices. These higher prices encourage greater extraction of energy products, even when the cost of extraction is rising because of diminishing returns. Even if extraction costs keep rising, the situation of ever-rising commodity prices cannot go on endlessly. At some point, prices become too high for workers to afford. Demand tends to fall at some point because workers at the bottom of the hierarchy find themselves “priced out” of buying goods such as houses and cars that would help maintain commodity demand.

What causes debt levels to stop rising? One reason why debt levels stop rising is that debt reaches absurd levels, making it difficult to repay debt with interest. Several examples of absurd debt levels are given in Slide 21. An additional example is excessive use of student loans. If incomes after student loans are not high enough, student debt may create a huge burden, preventing former students from buying homes and cars and starting families. The problem is that incomes after the educational experience are not sufficiently high to both pay back debt with interest and leave adequate funds for other needs.

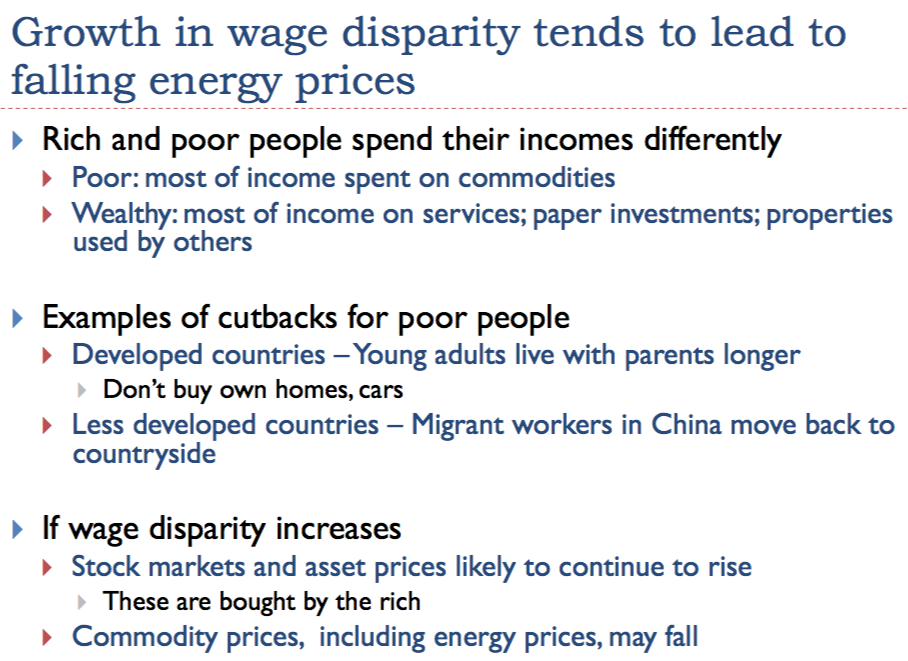

Growing wage disparity can also lead directly to falling energy prices:

Slide 22. Growing wage disparity tends to lead to falling energy prices.

Both growing wage disparity and lack of growth in debt are signs that an economy is not growing very fast–in some sense, that the economy is not hot enough. Some of the would-be workers tend to drop out of the system, because wages are not high enough to cover commuting and childcare expenses. In some sense, they “condense out,” similar to the way that water turns to ice when there is not enough heat in the system.

The situation with prices of fossil fuels is similar; low prices are a sign that the economy is not growing fast enough. The system is forcing a reduction in the production of many kinds of commodities, including fossil fuels, by reducing prices below the cost of production for quite a few producers. This situation can be thought of as some of the production “condensing out,” because the energy products consumed are not causing the world economy to grow fast enough to maintain a “hot” demand level.

More Thoughts on Energy Prices and Debt Levels

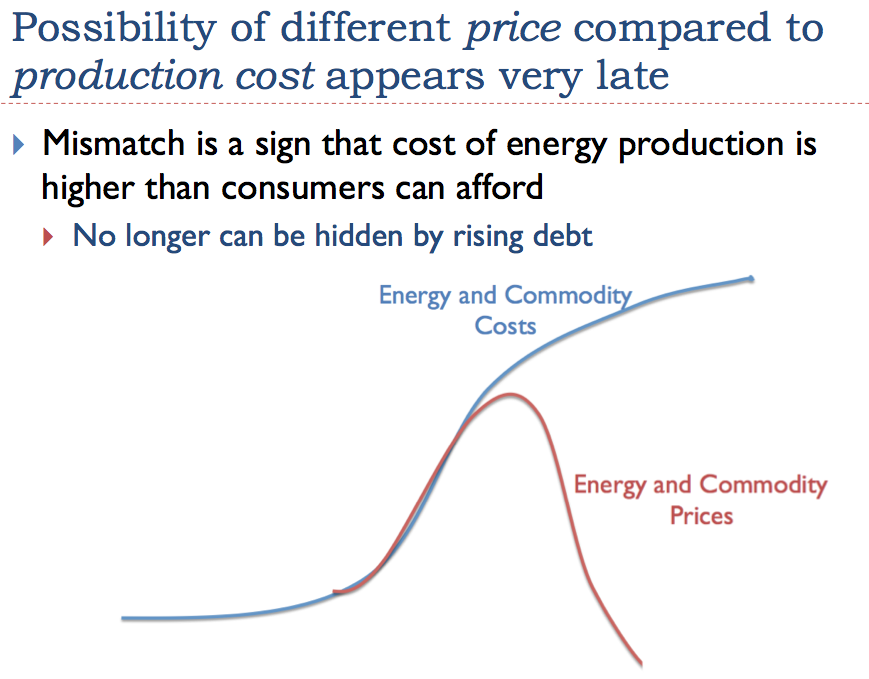

Slide 24. Use of debt permits two different valuations of worth of commodities.

The thing that is confusing is that for many years, energy and commodity costs were very similar to energy and other commodity prices. It has been only very recently–when prices rose too high for consumers to afford–that the difference has appeared.

Slide 25. Possibility of different price compared to production cost appears very late.

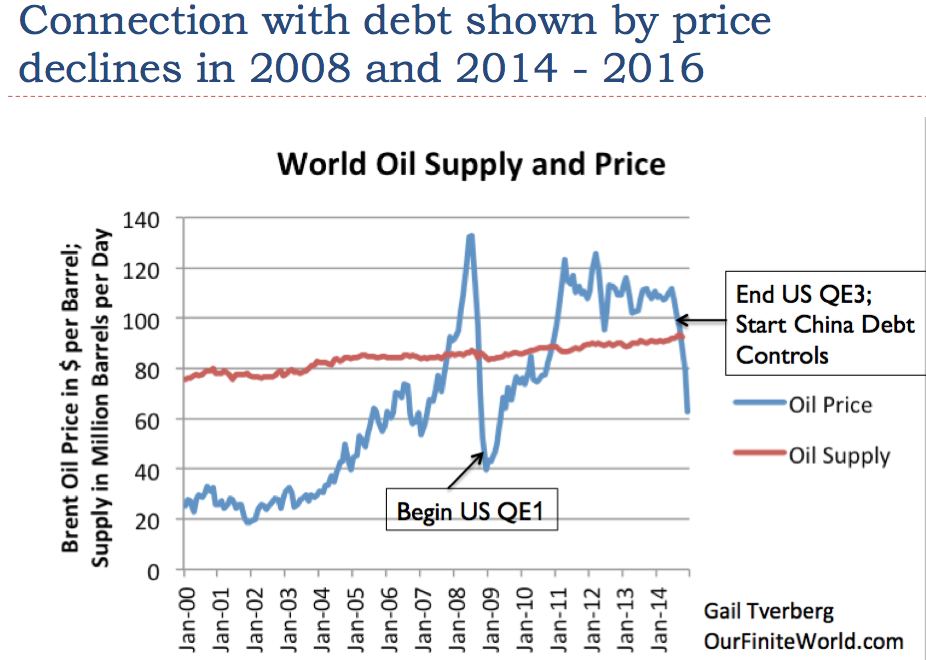

Looking at historical data in Slide 26, we can see two recent sharp drops in oil prices. Both occurred when debt levels were no longer rising.

Slide 26. Connection of debt with oil prices is shown by two sharp declines.

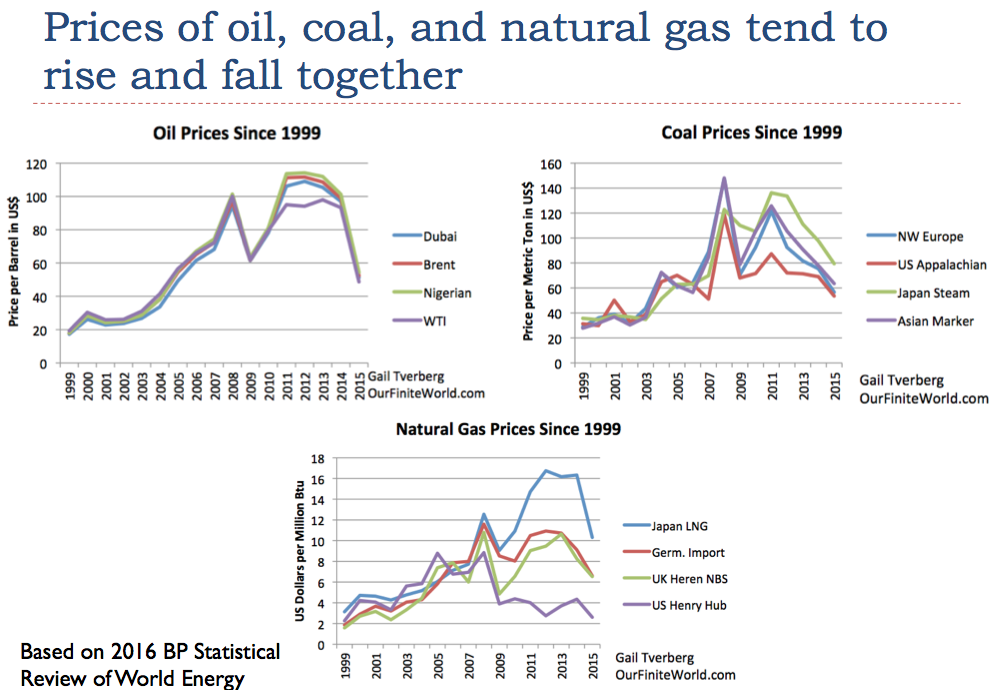

In fact, prices of oil, coal, and natural gas tend to rise and fall together–just as we would expect, if they are all responding to the same changes in debt levels, and indirectly, the same changes in world economic growth rates.

Slide 27. Prices of oil, call and natural gas tend to rise and fall together.

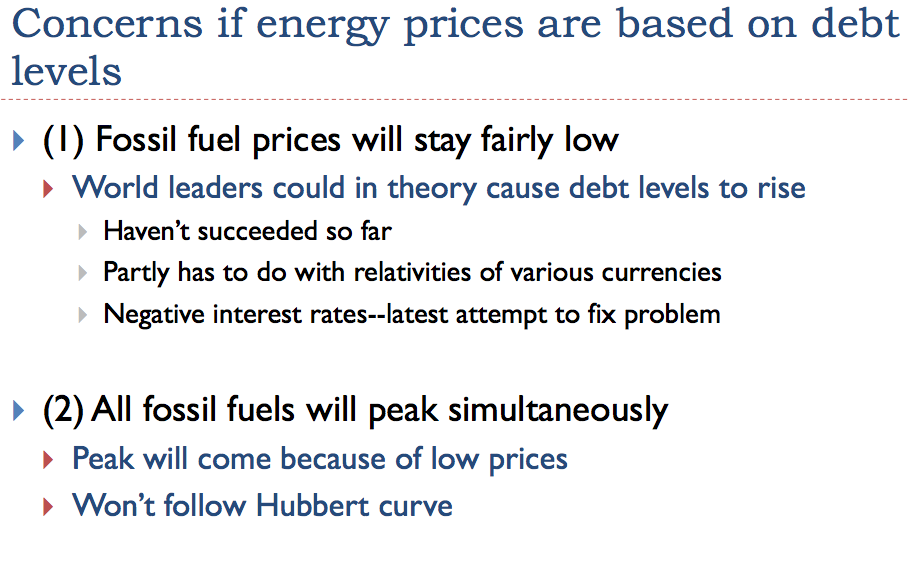

If energy prices are based on debt levels, our concern should be that all fossil fuels will peak within a few years of each other. The cause of the peak will be low prices, not “running out” of energy products.

Slide 28. Concerns if energy prices are based on debt levels

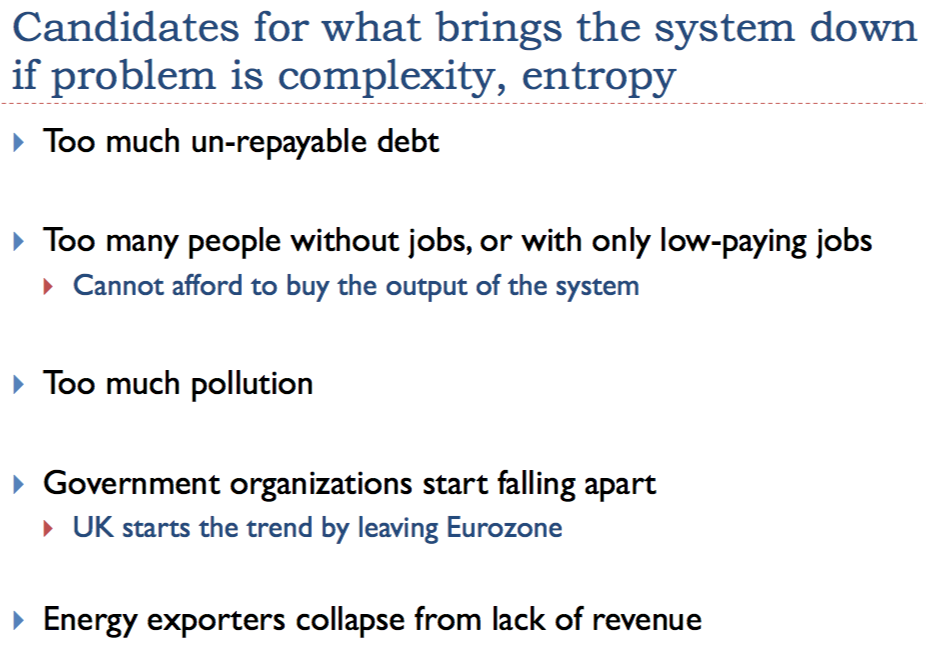

In fact, the problems of the economy may be quite different from “running out.”

Slide 31. Candidates for what really brings the system down.

Supplemental Information on Income Disparity

A few slides giving additional information on income disparity are shown as slides 38-40. Please check the end of my presentation for these.

Conclusion

One topic I did not specifically discuss in this presentation is the possibility of slowing world economic growth. If we are seeing falling world energy consumption per capita, it should not be surprising if world GDP growth per capita is falling as well. I have talked about the link between energy consumption and GDP growth many times, including in my paper, Oil Supply Limits and the Continuing Financial Crisis.

It was not until I sat down to write up this presentation that I realized how closely the timing of the recent sharp drop of world oil prices corresponds with the decrease in world per capita energy consumption shown on Slide 4. World per capita energy consumption hit a peak in 2013, and dropped slightly in 2014, with a greater change in 2015. Mid-2014 is when oil prices began their major slide, so the timing of the two events matches up almost precisely. Thus, the drop in coal consumption may be resulting in low world economic growth, which in turn is holding down both oil and natural gas prices.

The apparent coincidence in timing may simply reflect the fact that the same forces that cause falling commodity prices are also causing low economic growth. Growing wage disparity and lack of growth in debt seem to be factors in causing both. If workers at the bottom of the hierarchy could better afford the output of the world economy, with or without additional debt, the world economy would have a better chance of growing.

I don’t see much hope for fixing a world whose economy is moving in the direction of shrinkage. Instead, the situation is likely to get worse, until the financial system collapses, or one of the issues shown on Slide 31 starts to become too great a problem.

I see the big push for renewables to be mostly a waste of time and resources. The major exception is perhaps hydroelectric, in parts of the world with good locations for new installations. EROI analyses are often used to justify renewables, but in my view (shown in the part of the presentation not discussed), EROI is too “blunt” a tool to properly evaluate resources that differ greatly in quality of output and in debt requirements. A major goal needs to be to maintain the functionality of the electric grid; evaluations of intermittent renewables should consider real-life experiences of other countries. For example, current pricing approaches seem to exacerbate the problem of falling wholesale electricity prices, and thus falling fossil fuel prices. (See this or this article.)

A major impediment to getting a rational discussion of the issues is the inability of a large share of the population to deal with what appears to be a potentially dire outcome. Textbook and journal editors recognize this issue, and gear their editorial guidelines accordingly. I was reminded of this again, when the question came up (again) of whether I would consider writing a book for a particular academic book publisher. The main thing I would need to do to make the book acceptable would be find a way of sidestepping any unpleasant outcome–or, better yet, I should come up with a “happily ever after” ending.

{kind=link}

{kind=link}