This past week, I gave a presentation to a group interested in a particular type of renewable energy–solar energy that is deployed in space, so it would provide electricity 24 hours per day. Their question was: how low does the production cost of electricity really need to be?

I gave them this two-fold answer:

1. We are hitting something similar to “Peak Oil” right now. The symptoms are the opposite of the ones that most people expected. There is a glut of supply, and prices are far below the cost of production. Many commodities besides oil are affected; these include natural gas, coal, iron ore, many metals, and many types of food. Our concern should be that low prices will bring down production, quite possibly for many commodities simultaneously. Perhaps the problem should be called “Limits to Growth,” rather than “Peak Oil,” because it is a different type of problem than most people expected.

2. The only theoretical solution would be to create a huge supply of renewable energy that would work in today’s devices. It would need to be cheap to produce and be available in the immediate future. Electricity would need to be produced for no more than four cents per kWh, and liquid fuels would need to be produced for less than $20 per barrel of oil equivalent. The low cost would need to be the result of very sparing use of resources, rather than the result of government subsidies.

Of course, we have many other problems associated with a finite world, including rising population, water limits, and climate change. For this reason, even a huge supply of very cheap renewable energy would not be a permanent solution.

This is a link to the presentation: Energy Economics Outlook. I will not attempt to explain the slides in detail.

Slide 1

Slide 2

Some people falsely believe that energy supplies are “only needed for industrial purposes.” Energy supplies are, in fact, needed for many things: cooking our food, keeping our homes warm, and creating the clothing we expect to wear. It would be impossible to feed, house, and clothe 7.3 billion people without supplemental energy of some kind.

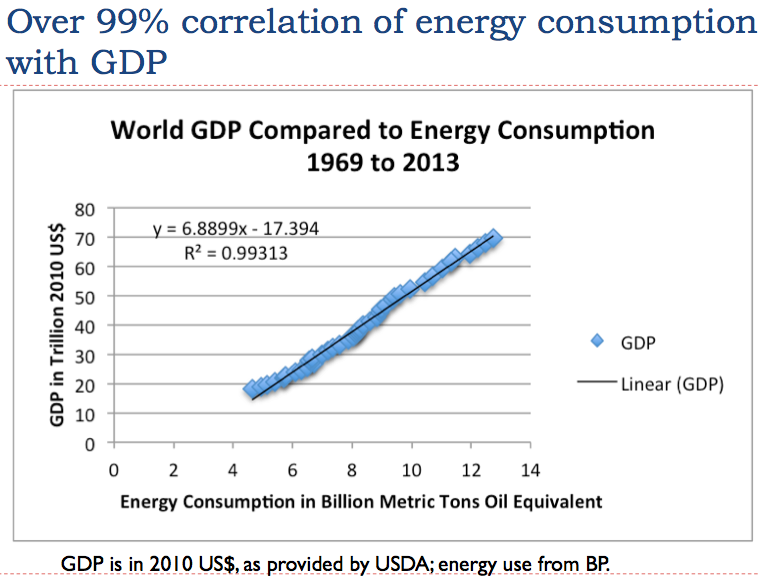

Slide 3

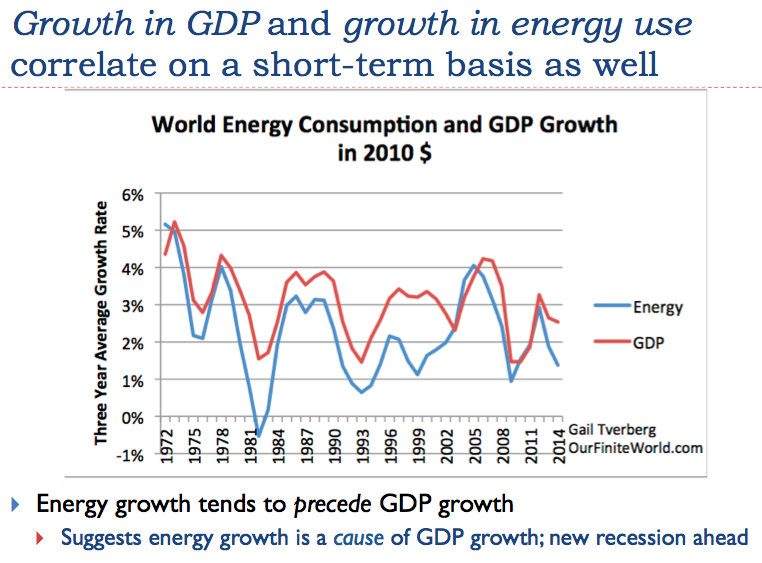

Slide 4

Slide 4 suggests that the world economy is heading into recession, because recent growth in the use of energy supplies is very low recently. Another sign that we are headed into recession is that fact that CO2 emissions fell in 2015. They usually don’t fall unless a global crisis exists. Emissions fell when the Soviet Union collapsed in 1991, and they fell during the economic crisis in 2008. Perhaps the world economy is hitting headwinds that are not being picked up well in conventional calculations of GDP growth.

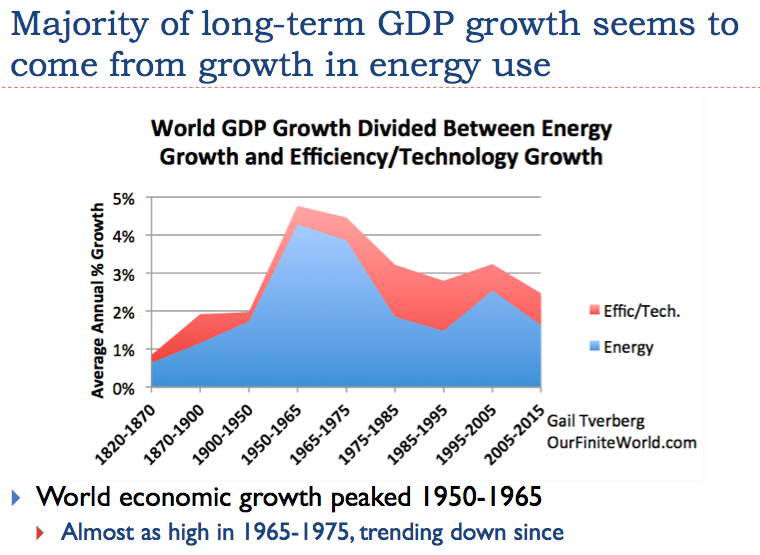

Slide 5

Slide 5 shows a chart I put together, using data from several different sources, showing how growth in energy consumption has compared with growth in GDP. Growth in GDP tends to be somewhat higher than growth in energy consumption.

Economic growth (and growth in energy use) was low prior to 1950. There was a big jump in economic growth immediately after World War II, in the 1950-65 period. There was almost as much growth in the 1965- 75 period. Since 1975, economic growth has generally been slowing.

Slide 6

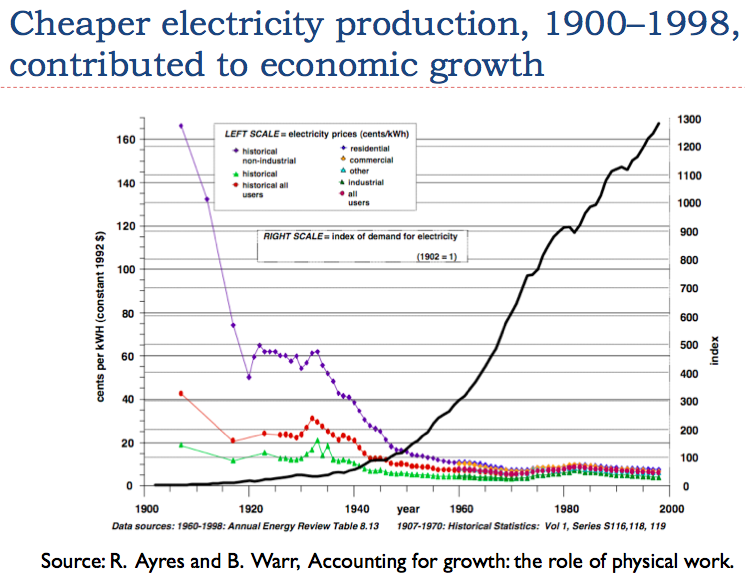

Between the years 1900 and 1998, the use of electricity rose (black line) as the cost of electricity fell (purple, red, and green lines). Electricity consumption could rise because it was becoming more affordable. Rising electricity consumption allowed the economy to make more goods and services. Workers (with the use of electricity) were becoming more efficient, so wages could rise. With higher wages, workers could afford more products that used electricity, such as electric lights for their homes and radios.

If electricity prices had risen instead of fallen, it seems doubtful that this pattern of rising consumption could have taken place.

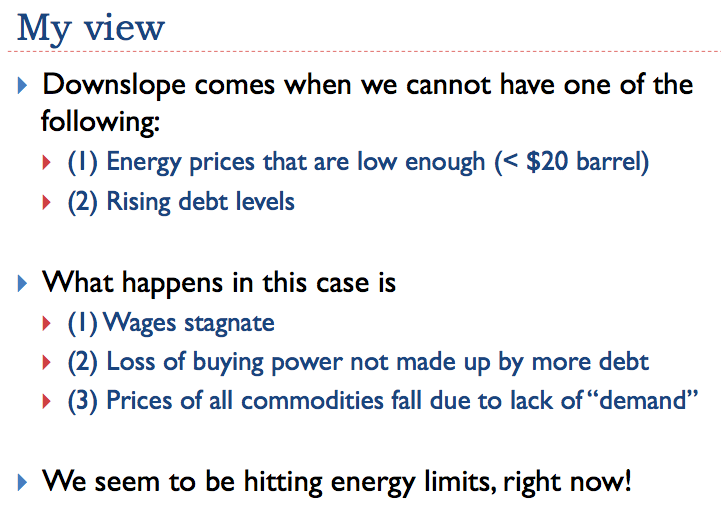

Slide 7

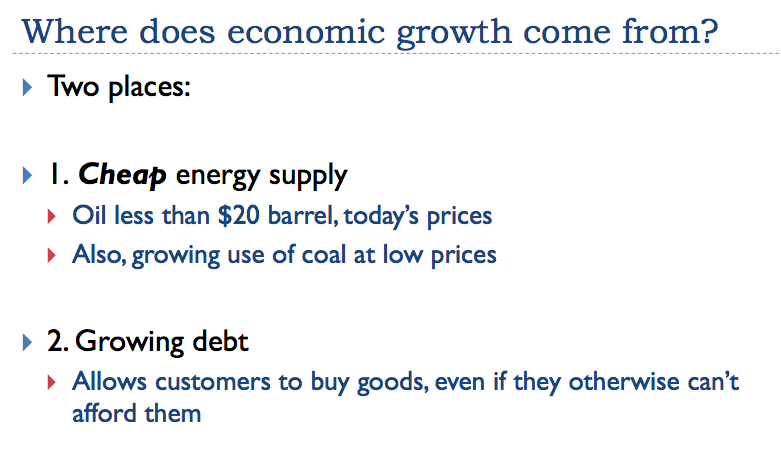

The comments in Figure 7 represent my own view. It is based on both theoretical considerations and historical relationships. Many who have studied the economy believe that energy is important for economic growth. In my view, the real need is for cheap-to-produce energy, not just any energy. If cheap energy is not really available, then adding more debt can somewhat make up for the high cost of energy production.

Debt is important because it makes goods affordable that would not otherwise be affordable. For example, having a loan for a house or a car makes a huge difference regarding whether such an item is affordable.

Even when energy products are cheap, debt seems to be needed to get oil or coal out of the ground, or to make a new device such as a wind turbine. Part of the problem is the cost of the capital equipment needed to extract the oil or coal, or the cost of the wind turbines themselves. Another part of the problem is paying for factories to make devices that use the energy product. A third problem is making it possible for users to afford the end products, such as houses and cars. It is much easier to borrow the money for a new tractor, and pay the loan off as the tractor is put to use, than it is to save money in advance, using only the funds earned when farming with simple hand-held tools.

Slide 8

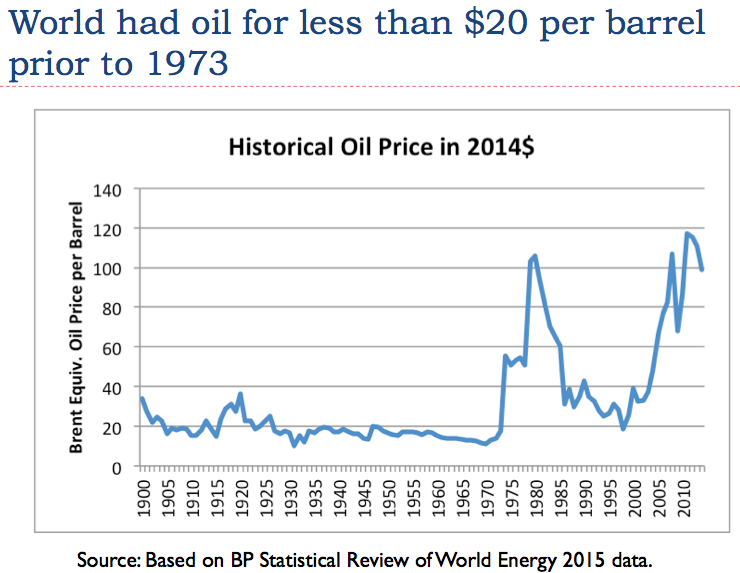

I mentioned the need for $20 per barrel oil on Slide 7. This is a very inexpensive price. Slide 8 shows that the only time when oil prices were that low was prior to the mid-1970s. The cost of oil production is now far above $20 per barrel. The sales price now is about $37 per barrel. This is below the price producers need, but still above my target price level.

Slide 9

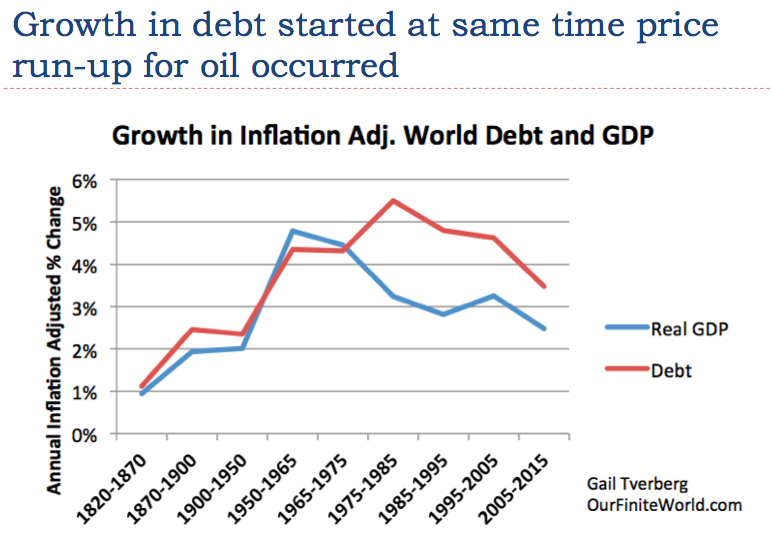

Slide 9 explains where I got my $20 per barrel price target. Back prior to 1975–in other words, back when oil prices were generally low, $20 per barrel or less–the increase in debt more or less corresponded to the growth in GDP. Once prices rose above $20 per barrel, the amount of debt needed to produce a given amount of GDP growth rose dramatically.

Slide 10

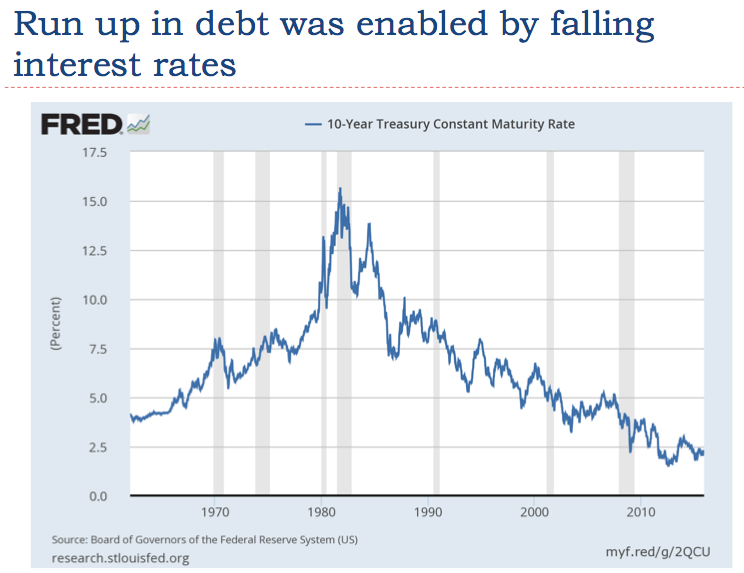

Slide 10 shows interest rates for US debt with 10-year maturity. These interest rates often underlie mortgage rates. As interest rates fall, homeowners can afford increasingly expensive homes. If shorter-term interest rates fall as well, auto loans become cheaper too.

Slide 11

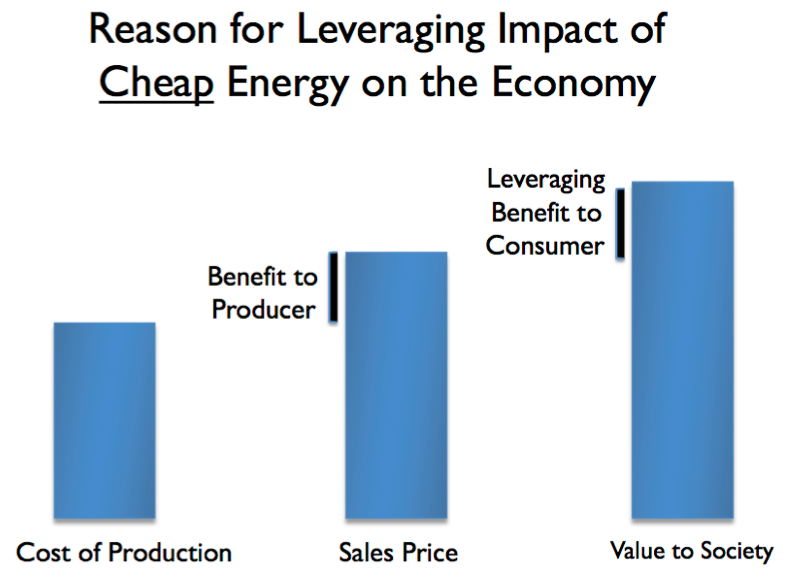

The value to society of a barrel of oil is determined by how many miles it can make a diesel truck go, or how far it can make an airplane fly. This value to society is more or less fixed. The only change is the small increment each year from efficiency changes, making a barrel of oil “go farther.”

In the 2000-14 period, the cost of new oil production was increasing very rapidly–by more than 10% per year, by some estimates. The rising cost of oil production occurred much more quickly than efficiency changes. The result was a falling difference between the value to society and the cost of production. When oil prices are high, oil-importing nations tend to suffer recession. When oil prices are low, oil-exporting nations find it hard to collect enough taxes to support their many programs.

Slide 12

The fact that we need energy for economic growth means that we somehow must obtain this energy, even if doing so costs more. The big run-up in oil prices is a major reason for the historical run-up in debt levels. China’s big build-out of homes, roads, and factories was also financed by debt.

The higher cost of oil affects many things that we don’t think are related, including the cost of building new homes, the cost of building cars, and the cost of building roads. As consumers are forced to buy increasingly expensive homes and cars, and as governments find that the building of roads is increasingly expensive, more debt is used. The terms of loans are often longer as well, to hold down monthly costs.

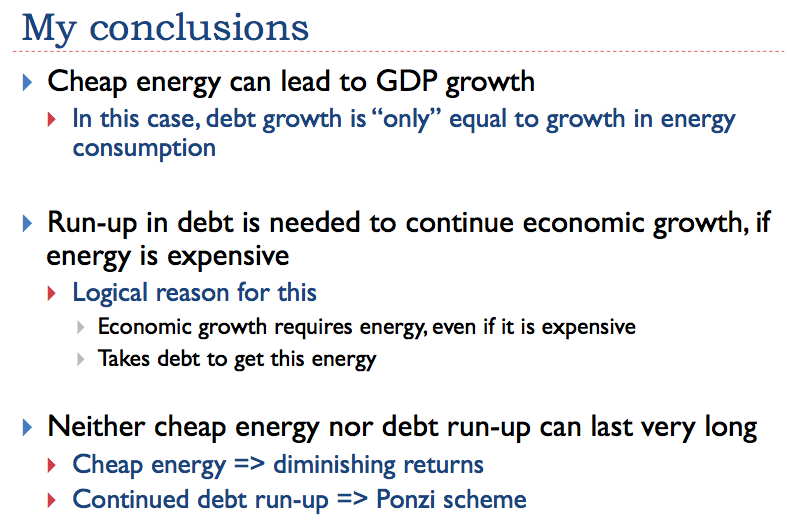

If we still had cheap oil, this oil by itself could provide a “lift” to the economy. An increasing amount of debt can “sort of” compensate for the absence of cheap oil.

The problem we encounter is that neither cheap energy nor the continued run-up of debt is sustainable. Cheap energy tends to change to expensive energy, because we use the cheapest sources first. The continued debt run-up becomes more and more difficult to handle, unless interest rates fall lower and lower. At some point, interest rates can’t fall enough, and the whole pile of debt tends to collapse, like a Ponzi scheme.

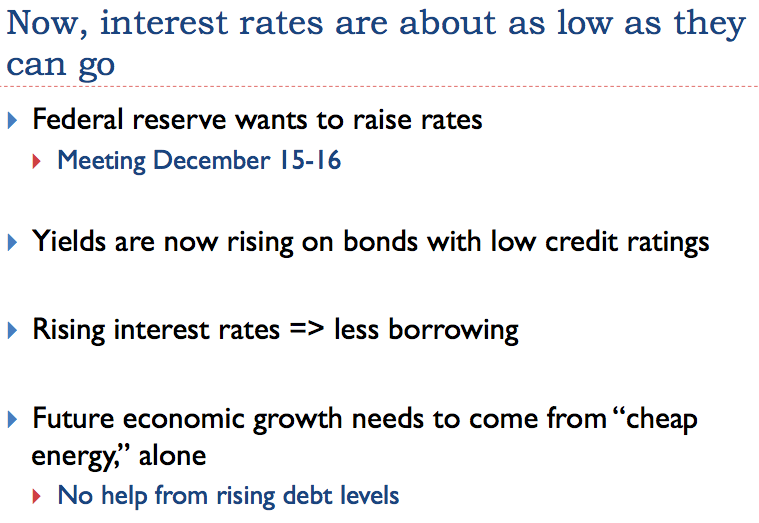

Slide 13

I gave this talk on December 15; the first increase in interest rates took place on December 16. With rising interest rates, we suddenly have “the prop” that was attempting to hold up economic growth taken away.

We need ever expanding debt–that is, debt rising faster than GDP levels–to try to keep the world economy growing, so that the whole pile of debt doesn’t fall over and collapse. If we are to have non-debt growth in the future (because we are reaching limits on debt), it needs to again come from cheap energy alone. We need to get back to something similar to the low-cost energy that fueled the economy before the debt run-up.

Slide 14

Most of us have heard the Peak Oil story, and assume it represents a reasonable view of where we are headed. I think it is close to 180 degrees off course.

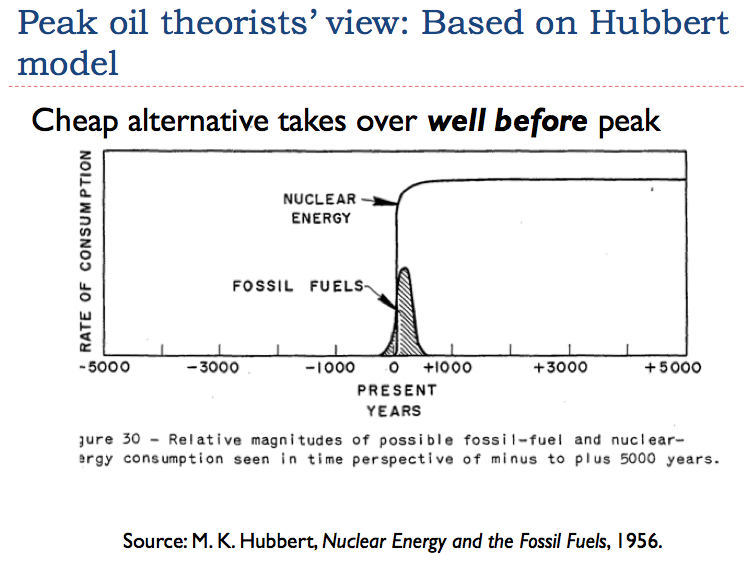

Slide 15

M. King Hubbert talked about a very special situation–a situation where another cheap, abundant fuel took over, before fossil fuels began to decline. In this particular situation (and only in this particular situation), it is reasonable to assume that production will follow a symmetric “Hubbert Curve,” with half of the production coming after the peak, and half beforehand. Otherwise, the down slope is likely to be much steeper.

Many peak oilers missed this important point. We certainly are not in a situation today where another very cheap fuel has taken over.

Slide 16

Slide 16 represents what I see as the predominant “Peak Oil” view of the oil limits situation. Some individuals will of course have different opinions.

Slide 17

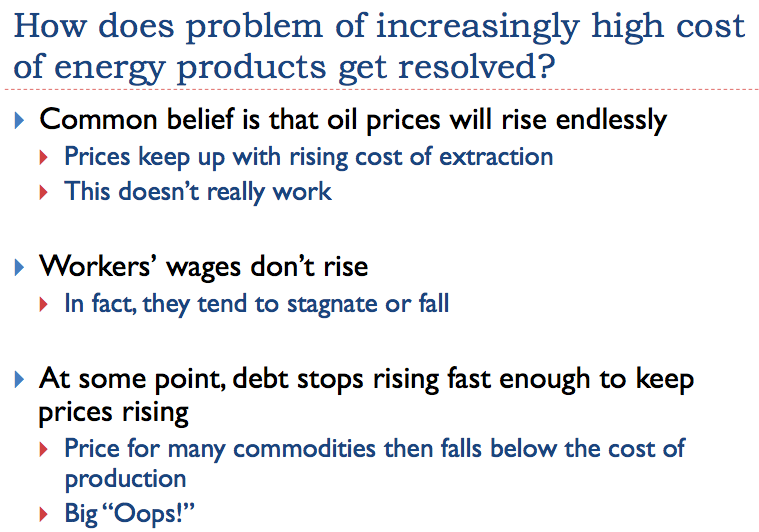

Peak oilers certainly did get part of the story right–at some point, the cost of oil extraction would rise. What they got wrong was how the whole scenario would play out. It turns out, it plays out pretty much the opposite of what most had supposed–that is, with stagnating wages, loss of buying power, and prices of all commodities falling because of lack of “demand.”

We seem to be hitting energy limits, right now. That is why debt is such a problem, and it is why prices of many commodities, including oil, are far too low compared to the cost of production.

Slide 18

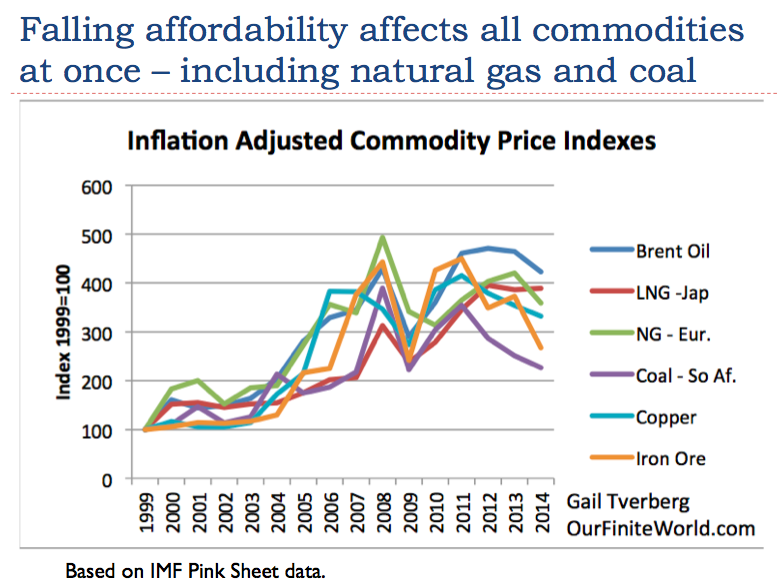

Slide 18 shows the fall of commodity prices up through 2014. The fall in commodity prices has continued in 2015 as well. The story we frequently hear is about low oil prices, but there is also a problem with low natural gas prices. Coal prices are low now too, and, in fact, many coal producers are near bankruptcy. Prices of iron ore, steel, copper, and many other metals are very low, as are prices of many kinds of staple foods traded internationally.

Slide 19

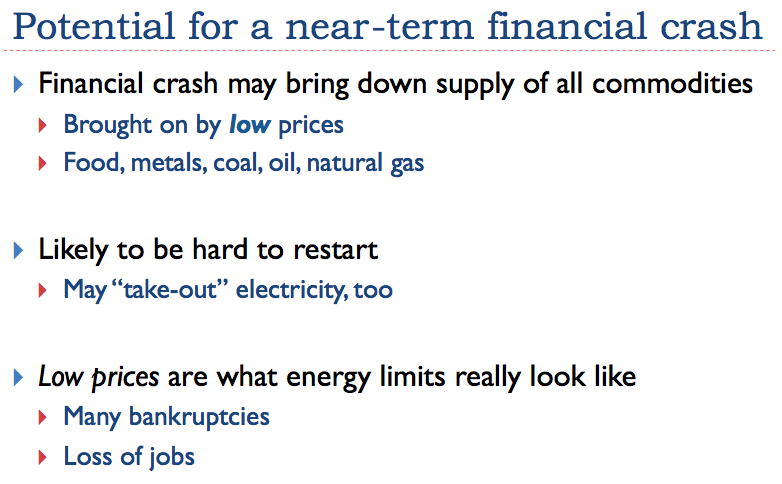

The problem with low commodity prices is that there are many loans that have been taken out to support their production. There is a significant chance of default, if prices remain low. Also, low commodity prices affect asset prices–for example, prices of coalmines, or prices of agricultural land. As the prices of commodities fall, the price of the land used to produce those commodities falls. When this happens, it becomes difficult to repay the loans on the property.

Slide 20

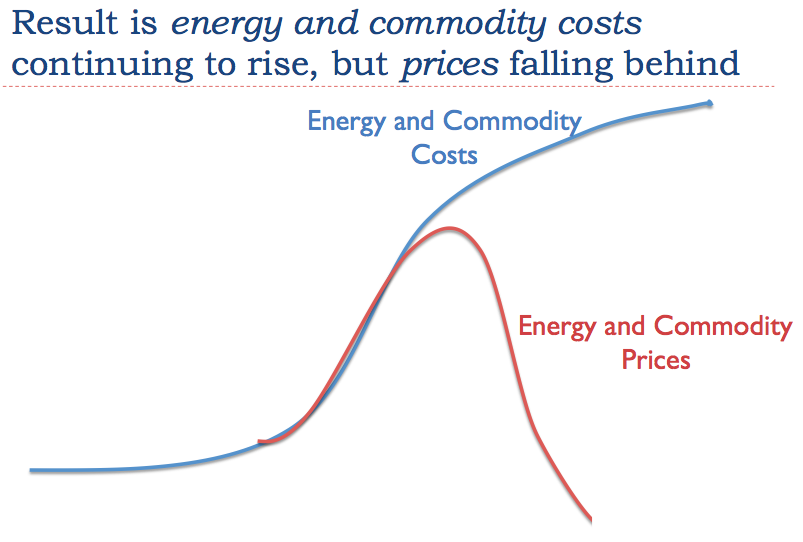

Peak Oilers were right about the cost of production continuing to rise. What they missed was the fact that prices would at some point fall behind the cost of production because of affordability issues. Low prices would then bring the economy down, as it did in the Depression in the 1930s, and in quite a few earlier collapses.

I think of increased demand, provided by debt, as being like a rubber band. Just as a rubber band can stretch for a while, the price of oil can rise for a while, fueled by more and more debt. At some point, debt can’t rise any higher–the rate of return on investments made using debt is too low, and defaults become too frequent. Instead of continuing to rise, commodity prices fall back. Market prices of commodities fall to much lower prices than the costs of production.

In order to get oil prices up higher, the wages of factory workers, restaurant workers, and other non-elite workers need to rise, so that they can afford to buy nice cars and nice homes. Commodities of many types are used both in making homes and cars, and in operating them.

Slide 21

If space solar (or for that matter, any renewable energy) is to be helpful, it needs to be very cheap, so that products made using renewable energy are affordable.

If the replacement energy source is cheap enough, perhaps there will not be a huge run-up in debt to GDP ratios, to finance the new devices used to provide electricity or other energy.

We are encountering problems now, so we need a replacement now, not 20 or 50 years from now.

Slide 22

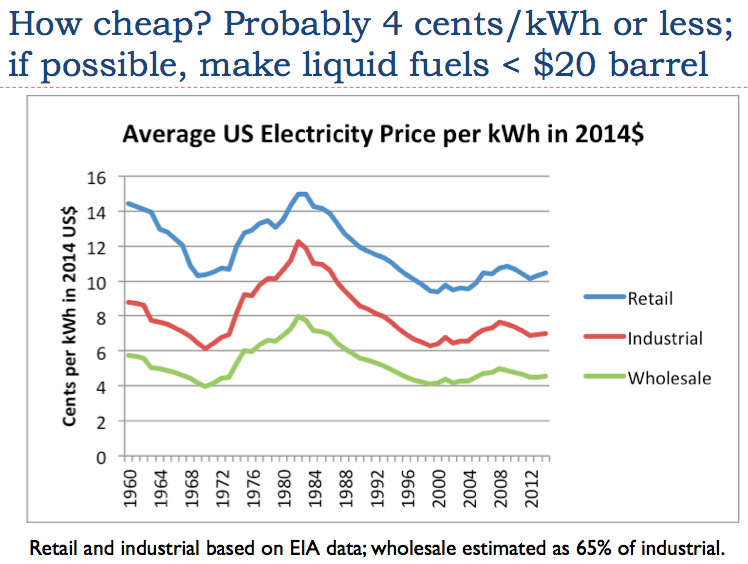

We cannot expect the cost of electricity production to be more than the current wholesale selling price of electricity. Thus, it needs to be four cents per kWh or less. Ideally, the price of electricity should be falling, as in Slide 6.

Another consideration is that we need to be able to operate our current vehicles using a liquid fuel, made with electricity, because of the time and materials involved in switching over to electric vehicles. This requirement likely reduces the maximum cost of electricity even below four cents per kWh.

Slide 23

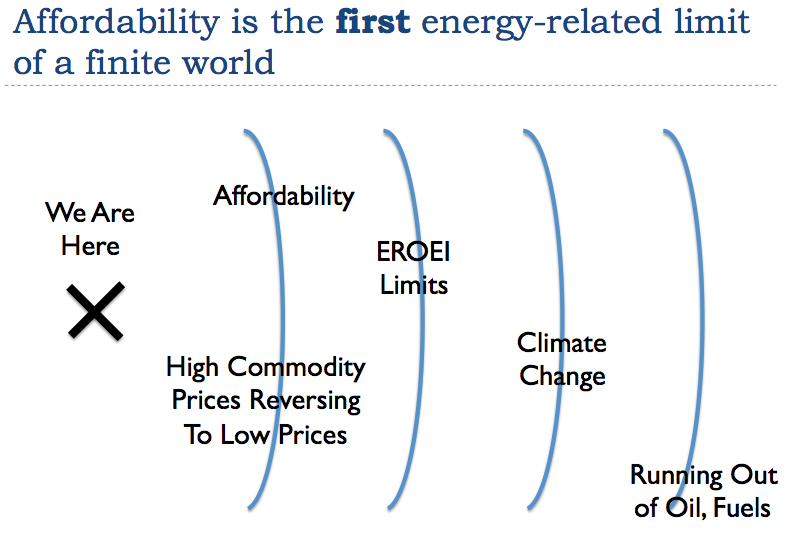

It is possible to run into many different kinds of limits, over a period of time. In my view, the first limit we reach is an affordability limit. We can tell we are hitting this limit when high prices reverse to low prices, as they have done since 2011. The fact that prices are continuing to fall is especially worrisome.

Slide 24

There has been a popular myth that it is OK for energy costs to rise. We will just choose the least costly of the high-priced alternatives. This approach doesn’t really work, because wages do not rise at the same time.

Also, we have to compete with other countries. If their energy costs are cheaper, their manufacturing costs are likely to be lower.

Slide 25

If conditions existed that allowed oil prices to rise endlessly (in other words, rising wages of non-elite workers together with debt that could spiral ever higher, as a percentage of GDP), we wouldn’t really have a problem–we could afford increasingly expensive substitutes. Unfortunately, the story of ever-rising oil prices is simply fiction. It is a pleasant story, but not really true. I explain some of the issues further in “Why ‘supply and demand’ doesn’t work for oil.”