The annual BP Statistical Review has come out, as usual in June. In this post we focus on the Asia Pacific region. This is important becausethe Australian government has offered the help of “Team Australia” to build the “Asian Century”. The question no one asks (or wants to ask) is how much oil there is to carry Asia through the decades to come. No one can give an answer of course but it is clear that if past oil consumption and production trends continue the region will slide into a huge oil crisis.

Overview

Oil production in the Asia Pacific peaked in 2010 (China offshore!) at 8.4 mb/d while consumption continued to increase to 30.9 mb/d.

Fig 1: Asia-Pacific oil production and consumption

The difference between consumption and production (net imports) is now 73% of consumption, up from 68% ten years ago.

Oil consumption changes

Let’s zoom into the last 10 years. Consumption growth dropped from 6.2% in 2009/10 to 1.5% in 2013/2014 but this is still an annual 440 kb/d. If this reduced consumption growth were to continue an extra 2.2 mb/d would be needed by 2020 and 4.4 mb/d by 2025.

Fig 2: Asia’s oil production and consumption changes since 2005

Since global crude oil production started to peak in 2005 (base year in above graph), Asia did remarkably well to suck additional oil out of the global market, around 6 mb/d

Fig 3: Asia’s oil consumption changes after 2005

The main drivers are China, India and Japan.

China’s consumption growth was running at an average of +430 kb/d pa over the last 10 years, but with huge variations during the financial crisis and the recovery year of 2010 when it peaked at 1.05 mb/d. In 2014 it was still +380 kb/d. If consumption growth continued at the levels of the last 3 years, China would need an additional 2 mb/d by 2020.

This is important to know because China’s share of consumption growth is 49% while India’s is just 15%. The rest, 36% comes from all other Asian countries.

Consumption decline can mainly be seen in Japan. But in 2012, fuel oil use and direct crude oil burn in power plants had to be increased after the Fukushima accident.

Fig 4: Asia’s incremental oil consumption 2005-2014

The big Asian consumers

In the following graphs, “net imports” means the difference between oil consumption and production.

Fig 5: China consumption vs production

Fig 6: India consumption vs production

Fig 7: Japan’s oil imports

Fig 8: South Korea’s oil imports

Fig 9: Singapore’s oil imports

5 South East Asian oil producers

Fig 10: Indonesia is in peak oil mode

..

Fig 11: Malaysia peaked in 2004 but remained on a bumpy plateau during the last 4 years

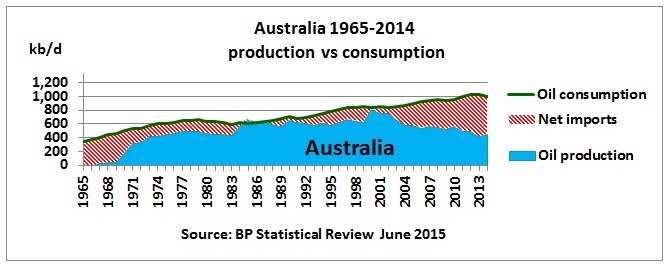

Fig 12: Australia peaked in 2000

Fig 13: Thailand’s oil production stagnated in the last 3 years

Fig 14: Vietnam has become a small net importer

All together now

Fig 15: South East Asia peaked in 2000 while consumption continues to grow

Conclusion:

It should be crystal clear that the much hyped Asian Century will last as long as increasing oil imports can keep the economies going. In a following post we’ll analyse where the imported oil is coming from.

Previous post:

18/6/2013

South East Asian oil producers – the widening gap between oil production and consumption