Falling barrels image via shutterstock. Reproduced at Resilience.org with permission.

A person might think that oil prices would be fairly stable. Prices would set themselves at a level that would be high enough for the majority of producers, so that in total producers would provide enough–but not too much–oil for the world economy. The prices would be fairly affordable for consumers. And economies around the world would grow robustly with these oil supplies, plus other energy supplies. Unfortunately, it doesn’t seem to work that way recently. Let me explain at least a few of the issues involved.

1. Oil prices are set by our networked economy.

As I have explained previously, we have a networked economy that is made up of businesses, governments, and consumers. It has grown up over time. It includes such things as laws and our international trade system. It continually re-optimizes itself, given the changing rules that we give it. In some ways, it is similar to the interconnected network that a person can build with a child’s toy.

Figure 1. Dome constructed using Leonardo Sticks

Thus, these oil prices are not something that individuals consciously set. Instead, oil prices reflect a balance between available supply and the amount purchasers can afford to pay, assuming such a balance actually exists. If such a balance doesn’t exist, the lack of such a balance has the possibility of tearing apart the system.

If the compromise oil price is too high for consumers, it will cause the economy to contract, leading to economic recession, because consumers will not be forced to cut back on discretionary expenditures in order to afford oil products. This will lead to layoffs in discretionary sectors. See my post Ten Reasons Why High Oil Prices are a Problem.

If the compromise price is too low for producers, a disproportionate share of oil producers will stop producing oil. This decline in production will not happen immediately; instead it will happen over a period of years. Without enough oil, many consumers will not be able to commute to work, businesses won’t be able to transport goods, farmers won’t be able to produce food, and governments won’t be able to repair roads. The danger is that some kind of discontinuity will occur–riots, overthrown governments, or even collapse.

2. We think of inadequate supply being the number one problem with oil, and at times it may be. But at other times inadequate demand (really “inadequate affordability”) may be the number one issue.

Back in the 2005 to 2008 period, as oil prices were increasing rapidly, supply was the major issue. With higher prices came the possibility of higher supply.

As we are seeing now, low prices can be a problem too. Low prices come from lack of affordability. For example, if many young people are without jobs, we can expect that the number of cars bought by young people and the number of miles driven by young people will be down. If countries are entering into recession, the buying of oil is likely to be down, because fewer goods are being manufactured and fewer services are being rendered.

In many ways, low prices caused by un-affordability are more dangerous than high prices. Low prices can lead to collapses of oil exporters. The Soviet Union was an oil exporter that collapsed when oil prices were down. High prices for oil usually come with economic growth (at least initially). We associate many good things with economic growth–plentiful jobs, rising home prices, and solvent banks.

3. Too much oil in too short a time can be disruptive.

US oil supply (broadly defined, including ethanol, LNG, etc.) increased by 1.2 million barrels per day in 2013, and is forecast by the EIA to increase by close to 1.5 million barrels a day in 2014. If the issue at hand were short supply, this big increase would be welcomed. But worldwide, oil consumption is forecast to increase by only 700,000 barrels per day in 2014, according to the IEA.

Dumping more oil onto the world market that it needs is likely to contribute to falling prices. (It is the excess quantity that leads to lower world oil prices; the drop in price doesn’t say anything at all about the cost of production of oil the additional oil.) There is no sign of a recent US slowdown in production either. Figure 2 shows a chart of crude oil production from the EIA website.

Figure 2. US weekly crude oil production through October 10, as graphed by the US Energy Information Administration.

4. The balance between supply and demand is being affected by many issues, simultaneously.

One big issue on the demand (or affordability) side of the balance is the question of whether the growth of the world economy is slowing. Long term, we would expect diminishing returns (and thus higher cost of oil extraction) to push the world economy toward slower economic growth, as it takes more resources to produce a barrel of oil, leaving fewer resources for other purposes. The effect is providing a long-term downward push on the price on demand, and thus on price.

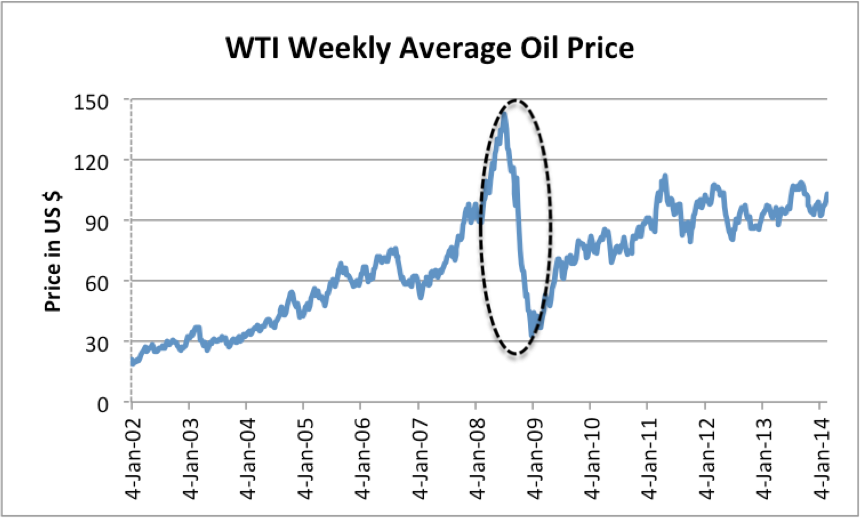

In the short term, though, governments can make oil products more affordable by ramping up debt availability. Conversely, the lack of debt availability can be expected to bring prices down. The big drop in oil prices in 2008 (Figure 3) seems to be at least partly debt-related. See my article, Oil Supply Limits and the Continuing Financial Crisis. Oil prices were brought back up to a more normal level by ramping up debt–increased governmental debt in the US, increased debt of many kinds in China, and Quantitative Easing, starting for the US in November 2008.

Figure 3. Oil price based on EIA data with oval pointing out the drop in oil prices, with a drop in credit outstanding.

In recent months, oil prices have been falling. This drop in oil prices seems to coincide with a number of cutbacks in debt. The recent drop in oil prices took place after the United States began scaling back its monthly buying of securities under Quantitative Easing. Also, China’s debt level seems to be slowing. Furthermore, the growth in the US budget deficit has also slowed. See my recent post, WSJ Gets it Wrong on “Why Peak Oil Predictions Haven’t Come True”.

Another issue affecting the demand side is changes in taxes and in subsidies. A change toward more taxes such as carbon taxes, or even more taxes in general, such as the Japan’s recent increase in sales tax, tends to reduce demand, and thus give a push toward lower world oil prices. (Of course, in the area with the carbon tax, the oil price with the tax is likely to be higher, but the oil price elsewhere around the world will tend to decrease to compensate.)

Many governments of emerging market countries give subsidies to oil products. As these subsidies are lessened (for example in India and in Brazil) the effect is to raise local prices, thus reducing local oil demand. The effect on world oil prices is to lower them slightly, because of the lower demand from the countries with the reduced subsidies.

The items mentioned above all relate to demand. There are several items that affect the supply side of the balance between supply and demand.

With respect to supply, we think first of the “normal” decline in oil supply that takes place as oil fields become exhausted. New fields can be brought on line, but usually at higher cost (because of diminishing returns). The higher cost of extraction gives a long-term upward push on prices, whether or not customers can afford these prices. This conflict between higher extraction costs and affordability is the fundamental conflict we face. It is also the reason that a lot of folks are expecting (erroneously, in my view) a long-term rise in oil prices.

Businesses of course see the decline in oil from existing fields, and add new production where they can. Examples include United States shale operations, Canadian oil sands, and Iraq. This new production tends to be expensive production, when all costs are included. For example, Carbon Tracker estimates that most new oil sands projects require a price of $95 barrel to be sanctioned. Iraq needs to build out its infrastructure and secure peace in its country to greatly ramp up production. These indirect costs lead to a high per-barrel cost of oil for Iraq, even if direct costs are not high.

In the supply-demand balance, there is also the issue of oil supply that is temporarily off line, that operators would like to get back on line. Libya is one obvious example. Its production was as much as 1.8 million barrels a day in 2010. Libya is now producing 800,000 barrels a day, but was producing only 215,000 barrels a day in April. The rapid addition of Libya’s oil to the market adds to pricing disruption. Iran is another country with production it would like to get back on line.

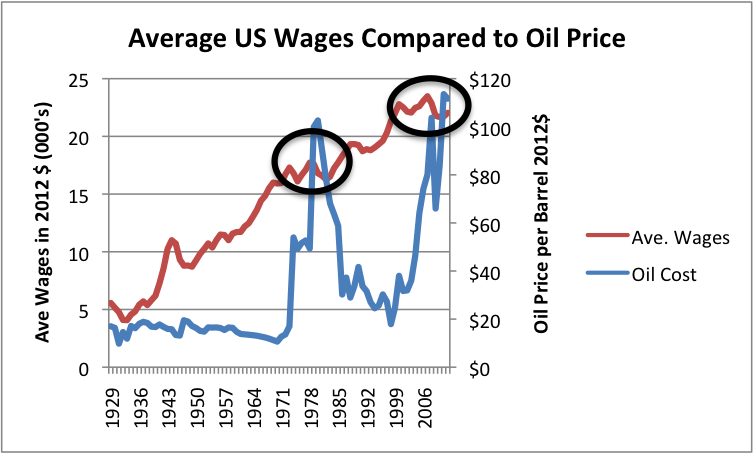

5. Even what seems like low oil prices today (say, $85 for Brent, $80 for WTI) may not be enough to fix the world’s economic growth problems.

High oil prices are terrible for economies of oil importing countries. How much lower do they really need to be to fix the problem? Past history suggests that prices may need to be below the $40 to $50 barrel range for a reasonable level of job growth to again occur in countries that use a lot of oil in their energy mix, such as the United States, Europe, and Japan.

Figure 4. Average wages in 2012$ compared to Brent oil price, also in 2012$. Average wages are total wages based on BEA data adjusted by the CPI-Urban, divided total population. Thus, they reflect changes in the proportion of population employed as well as wage levels.

Thus, it appears that we can have oil prices that do a lot of damage to oil producers (say $80 to $85 per barrel), without really fixing the world’s low wage and low economic growth problem. This does not bode well for fixing our problem with prices that are too low for oil producers, but still too high for customers.

6. Saudi Arabia, and in fact nearly all oil exporters, need today’s level of exports plus high prices, to maintain their economies.

We tend to think of oil price problems from the point of view of importers of oil. In fact, oil exporters tend to be even more affected by changes in oil markets, because their economies are so oil-centered. Oil exporters need both an adequate quantity of oil exports and adequate prices for their exports. The reason adequate prices are needed is because most of the sales price of oil that is not required for investment in oil production is taken by the government as taxes. These taxes are used for a variety of purposes, including food subsidies and new desalination plants.

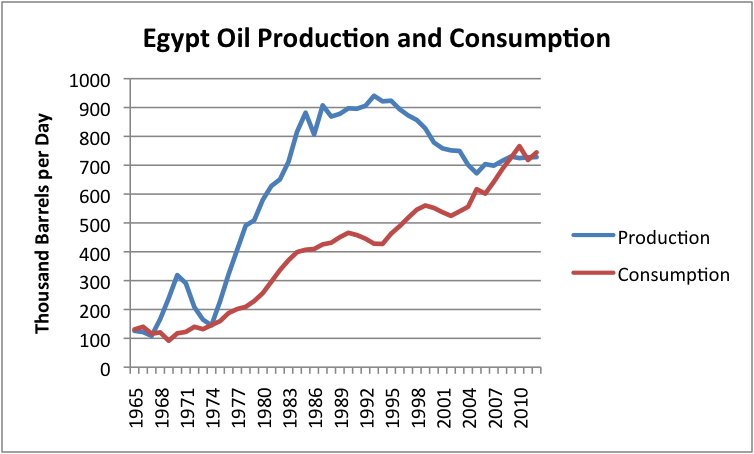

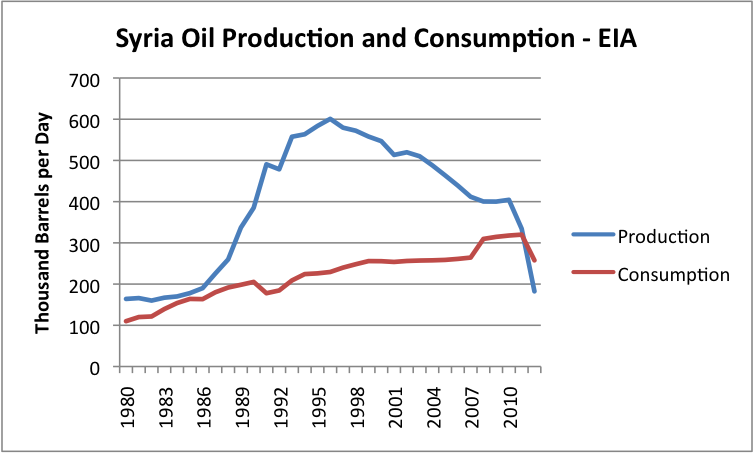

A couple of recent examples of countries with collapsing oil exports are Egypt and Syria. (In Figures 5 and 6, exports are the difference between production and consumption.)

Figure 5. Egypt’s oil production and consumption, based on BP’s 2013 Statistical Review of World Energy data.

Figure 6. Syria’s oil production and consumption, based on data of the US Energy Information Administration.

Saudi Arabia has had flat exports in recent years (green line in Figure 7). Saudi Arabia’s situation is better than, say, Egypt’s situation (Figure 5), but its consumption continues to rise. It needs to keep adding production of natural gas liquids, just to stay even.

Figure 7. Saudi oil production, consumption and exports based on EIA data.

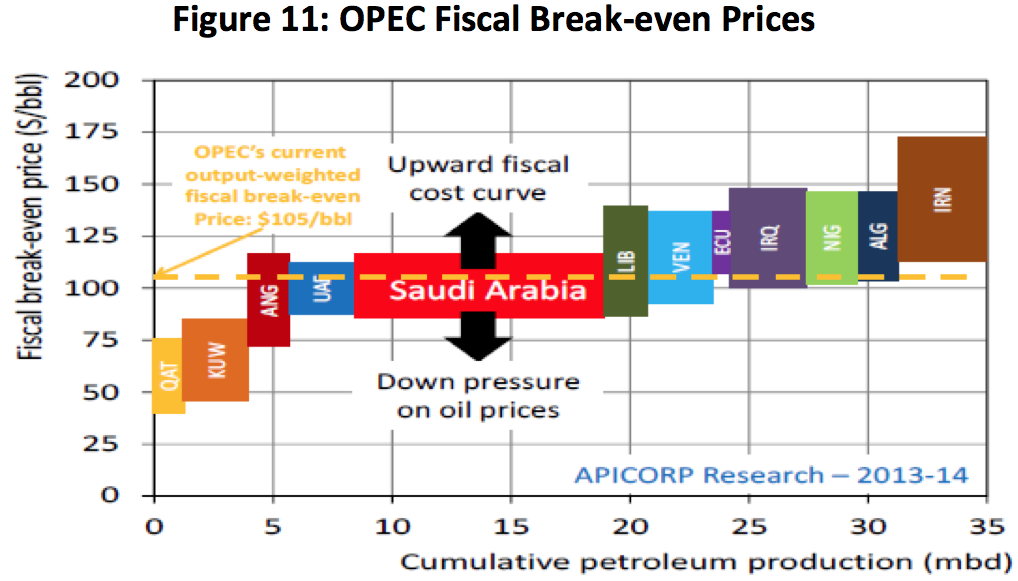

As indicated previously, Saudi Arabia and other exporting countries depend on tax revenues to balance their budgets. Figure 8 shows one estimate of required oil prices for OPEC countries to balance their budgets in 2104, assuming that the quantity of exported oil is pretty much unchanged from 2013.

Figure 8. Estimate of OPEC break-even oil prices, including tax requirements by parent countries, from APICORP.

Based on Figure 8, Qatar and Kuwait are the only OPEC countries that would find $80 or $85 barrel oil acceptable, assuming the quantity of exports remains unchanged. If the quantity of exports drops, prices would need to be even higher.

Saudi Arabia has set aside funds that it can tap temporarily, so that it can withstand a lower oil price. Thus, it has the ability to withstand low prices for a year or two, if need be. Its recent price-cutting may be an attempt to “shake out” producers who have less-deep pockets when it comes to weathering low prices for a time. Almost any oil producer elsewhere in the world might be in that category.

7. The world really needs all existing oil production, plus more, if the world economy is to grow.

It takes oil to transport goods, and it takes oil to operate agricultural and construction equipment. Admittedly, we can cut back world production oil production with lower price, but this gets us into “a heap of trouble”. We will suddenly find ourselves less able to do the things that make the economy function. Governments will stop fixing roads. Services we take for granted, like long distance flights, will disappear.

A lot of people have a fantasy view of a world economy operating on a much smaller quantity of fossil fuels. Unfortunately, there is no way we can get there by way of a rapid drop in oil prices. In order for such a change to take place, we would have to actually figure out some kind of transition by which we could operate the world economy on a lot less fossil fuel. Meeting this goal is still a very long ways away. Many people have convinced themselves that high oil prices will help make this transition possible, but I don’t see this as happening. High prices for any kind of fuel can be expected to lead to economic contraction. If transition costs are high as well, this will make the situation worse.

The easiest way to reduce consumption of oil is by laying off workers, because making and transporting goods requires oil, and because commuting usually requires oil. As a result, the biggest effect of a cutback on oil production is likely to be huge job layoffs, far worse than in the Great Recession.

8. The cutback in oil supply due to low prices is likely to occur in unexpected ways.

When oil prices drop, most production will continue as usual for a time because wells that have already been put in place tend to produce oil for a time, with little added investment.

When oil production does stop, it won’t necessarily be from high-cost production, because relative to current market prices, a very large share of production is high-cost. What will tend to happen is that production that has already been “started” will continue, but production that is still “in the pipeline” will wither away. This means that the drop in production may be delayed for as much as a year or even two. When it does happen, it may be severe.

It is not clear exactly how oil from shale formations will fare. Producers have leased quite a bit of land, and in some cases have done imaging studies on the land. Thus, these producers have quite a bit of land available on which a share of the costs has been prepaid. Because of this prepaid nature of costs, some shale production may be able to continue, even if prices are too low to justify new investments in shale development. The question then will be whether on a going-forward basis, the operations are profitable enough to continue.

Prices for new oil development have been too low for many oil producers for many months. The cutback in investment for new production has already started taking place, as described in my post, Beginning of the End? Oil Companies Cut Back on Spending. It is quite possible that we are now reaching “peak oil,” but from a different direction than most had expected–from a situation where oil prices are too low for producers, rather than being (vastly) too high for consumers.

The lack of investment that is already occurring is buried deeply within the financial statements of individual companies, so most people are not aware of it. Dividends remain high to confuse the situation. By the time oil supply starts dropping, the situation may be badly out of hand and largely unfixable because of damage to the economy.

One big problem is that our networked economy (Figure 1) is quite inflexible. It doesn’t shrink well. Even a small amount of shrinkage looks like a major recession. If there is significant shrinkage, there is danger of collapse. We haven’t set up a new type of economy that uses less oil. We also don’t have an easy way of going backward to a prior economy, such as one that uses horses for transport. It looks like we are headed for “interesting times”.