In the current debate about the Nature article "The Fracking Fallacy," the discussion has focused on estimates of cumulative production of shale gas plays by the Energy Information Administration (EIA) and The Bureau of Economic Geology at the University of Texas (UT/BEG).

David Hughes provides another estimate in his recent post "Fracking Fracas: The Trouble with Optimistic Shale Gas Projections by the U.S. Department of Energy," a summary of his comprehensive study of all U.S. shale plays Drilling Down published by The Post Carbon Institute.

The Fracking Fallacy debate is important because it casts doubt on the reliability of government estimates of our natural gas supply. If U.S. gas production is in decline by the early 2020s as described in the Nature article, or sooner as I suspect, then important policy decisions about the export of natural gas and the retirement of coal-fired electric power plants have been based on questionable information.

Cumulative production estimates are interesting but do not address the economics of shale plays. Proven reserves provide a more meaningful estimate because they supposedly represent volumes of oil and gas that can be produced commercially at a particular price.

There are two categories of proven reserves: proven developed producing (PDP) and proven undeveloped (PUD) reserves. PDP reserves refer to volumes of oil and gas that have been proven by drilling a well, testing its production and projecting its estimated ultimate production (EUR). PUD reserves are those volumes of oil and gas that can beinferred to be commercial but have not yet been drilled and tested. PUD reserves are booked based on proximity to PDP reserves.

Considerable uncertainty exists about the commerciality of shale production because of the lack of long-term production history to validate the EUR. I doubt that much of PDP shale gas reserves are, in fact, commercial based on our economic analysis of the Marcellus, Haynesville, Barnett and Fayetteville shale plays. PUD reserves are even more questionable since they have not been tested by a well. These observations are confirmed by public filings of financial data to the Securities and Exhange Commission by companies involved in these plays. This data shows that most companies have negative free cash flow and have extremely high debt loads. In other words, they are losing money.

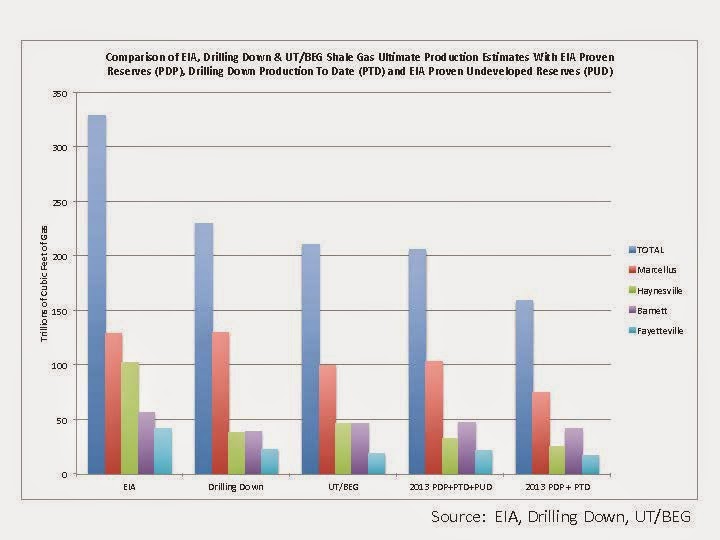

Proven reserves are, nevertheless, the best publicly-available measure of production potential from shale gas plays. The nearby chart and table compare the ultimate production estimates by the EIA, UT/BEG and Drilling Down (DD) with 2013 proven and proven undeveloped reserves published recently by the EIA.

(Click The Figure To Enlarge)

This data shows that both Drilling Down and UT/BEG cumulative production estimates are reasonably close to 2013 PDP reserves + PTD (Production To Date) + PUD reserves. The UT/BEG estimate is nearly identical with the PDP-PTD-PUD estimate except that Haynesville Shale production appears to be over-estimated. Drilling Down estimates appear to slightly under-estimate Barnett production and over-estimate Marcellus production compared to proven reserves.

The important take-away, of course, is that EIA appears to have over-estimated production for all of the plays by more than one-third (123 Tcf more) compared with total proven reserves. Its estimate for the Haynesville Shale play is more than three times as high (70 Tcf more) as proven reserves. EIA estimates for Barnett and Fayetteville are reasonably close to the PDP-PTD-PUD estimate. One has to wonder whether the people who do these production estimates for the EIA talk to the people in their own organization who do the reserve accounting.

The implication is that government estimates of shale gas supply appear to be highly optimistic compared with two studies by credible sources who I believe have done a much more thorough job than EIA of analyzing the production data by evaluating every individual well in the plays. All three estimates are probably optimistic because they use EIA price forecasts that I believe are too low.

How the SEC justifies approving reserves that financial data from the companies involved shows is non-commercial is a fascinating subject for another inquiry.

The shale gas success story of multi-decade abundance is at odds with the findings of the Bureau of Economic Geology and David Hughes’ work with The Post-Carbon Institute. The story stresses success based on resource estimates but not reserves, production volumes but not the cost of that production, the benefits of technology but not its price, and claims of profit that exclude important expenses.

The government and press accept this story because it paints a picture that fulfills so many aspirations of energy independence, U.S. re-emerging political strength, dominance in energy affairs and economic growth that warning signs of potential risk have so far been ignored.

Shale gas has provided the United States with a decade of supply that was not recognized as recently as 2005. That is a good thing. However, it probably represents a hiatus in the decline of U.S. gas reserves rather than a fundamental change in energy supply.

Drilling rig teaser image via shutterstock. Reproduced with permission at Resilience.org.