NOTE: Images in this archived article have been removed.

What is correct way to model the future course of energy and the economy? There are clearly huge amounts of oil, coal, and natural gas in the ground.

With different approaches, researchers can obtain vastly different indications. I will show that the real issue is most researchers are modeling the wrong limit.

Most researchers assume that the limit that they should be concerned with is the amount of oil, coal, and natural gas in the ground. This is the wrong limit. While in theory we will eventually hit this limit, because of the way fossil fuels are integrated into the rest of the economy, we hit financial limits much earlier. These financial limits include lack of investment capital, inability of governments to collect enough taxes to fund their programs, and widespread debt defaults.

One of the things I show in this post is that Economic Growth is a positive feedback loop that is enabled by cheap energy sources. (Economists have postulated that Economic Growth is permanent, and has no connection to energy sources.) Economic Growth turns to economic contraction as the cost of energy extraction (broadly defined) rises. It is the change in this feedback loop that leads to the financial problems mentioned above. These effects tend to lead to collapse over a period of years (perhaps 10 or 20, we really don’t know), rather than a slow decline which is easily mitigated.

If, indeed, most analysts are concerned about the wrong limit, this has huge implications for energy policy:

1. Climate change models include way too much CO2 from fossil fuels. Lack of investment capital will bring down production of all fossil fuels in only a few years. The amounts of fossil fuels included in climate change models are based on “Demand Model” and “Hubbert Peak Model” estimates of fossil fuel consumption (described in this post), both of which tend to be far too high. This is not to say that the climate isn’t changing, and won’t continue to change. It is just that excessive fossil fuel consumption needs to move much farther down our list of problems contributing to future climate change.

2. It becomes much less clear whether high-priced replacements for fossil fuels are worthwhile. In theory, they might allow a particular economy to have electricity for a while longer after collapse, if the whole system can be kept properly repaired. Offsetting this potential benefit are several drawbacks: (a) they make the economy with the high-priced replacements less competitive in the world marketplace, (b) they tend to run up debt, increase government spending, and decrease discretionary income of citizens, all limits we are reaching, and (c) they tend to push the economic cycle more quickly toward contraction for the country purchasing the high-priced renewables.

3. A large share of academic writing is premised on a wrong understanding of the real limits we are reaching. Since writers base their analyses on the wrong analyses of previous writers, this leads to a nearly endless supply of misleading or wrong academic papers.

This post is related to a recent post I wrote, The Real Oil Extraction Limit, and How It Affects the Downslope.

Types of Forecasting Models

There are three basic ways of making forecasts regarding future energy supply and related economic growth:

1. “Demand Based” Approaches. In this method, the analyst first decides what future GDP will be, and uses that estimate, together with past relationships, to “work backwards” to figure out how much energy supply will be needed in the future. The expected needed future energy supply is then divided up among various types of fuels, giving more of the growth to types that are favored, and less to other types. Very often, estimates of growth in energy efficiency, growth in “renewables,” and growth in the amount of GDP that can be generated with a given amount of energy supply are included in the model as well.

This method is by far the most common approach for forecasting expected future energy supply, especially at high levels of aggregation. One advantage of this method is that can provide almost any answer the analyst wants. Governments are paying for reports such as the EIA and IEA forecasts, and oil companies are paying for forecasts such as those by BP,Shell, and Exxon-Mobil. Both governments and oil companies prefer reports that say that everything will be fine for the foreseeable future. Demand Based approaches are good for producing such reports.

Another advantage of this approach is that the analysts don’t have to think about pesky details like where all of the investment capital will come from, or how large an improvement in the ratio of GDP to energy consumption can actually occur. They can simply make assumptions and point out that the forecast won’t come true if the assumptions don’t hold.

2. “Hubbert Peak Model”. This model is based on an interpretation of what M. King Hubbert wrote (for example, Nuclear Energy and the Fossil Fuels, 1956) . The basic premise of this model is that future supply of oil, coal, or gas will tend to drop slowly after 50% (or somewhat more) of the fuel supply potentially available with current technology has been extracted.

In fact, we don’t really know how much oil or coal or natural gas will be extracted in the future–we just know how much looks like it might be extracted, if everything goes well–if there is plenty of investment capital, if the credit system works as planned, and if the government is able to collect enough tax revenue to fund all of its promises, including maintaining roads and offering benefits to the unemployed.

What most people miss is the fact that the world economy is a Complex Adaptive System, and energy supply is part of this system. If there are diminishing returns with respect to energy supply–evidenced by the rising cost of extraction and distribution–then this will affect the economy in many ways simultaneously. The limit we are reaching is not that oil (or coal or natural gas) extraction will run out; it is that economic system will at some point seize up, and rapidly contract. The Hubbert Peak Method shows how much fuel might be extracted in each future year if the economy doesn’t seize up because of financial problems. The estimate produced by the Hubbert Peak Method removes some of the upward bias of the Demand Model approach, but it still tends to give forecasts that are higher than we can really expect.

3. Modeling How the Economy Actually Works. This approach is much more labor-intensive than the other two approaches, but is the only one that can be expected to give an answer that is in the right ballpark of being correct with respect to future economic growth and energy consumption. Of course, observing signs of oncoming collapse can also give an indication that we are nearing collapse.

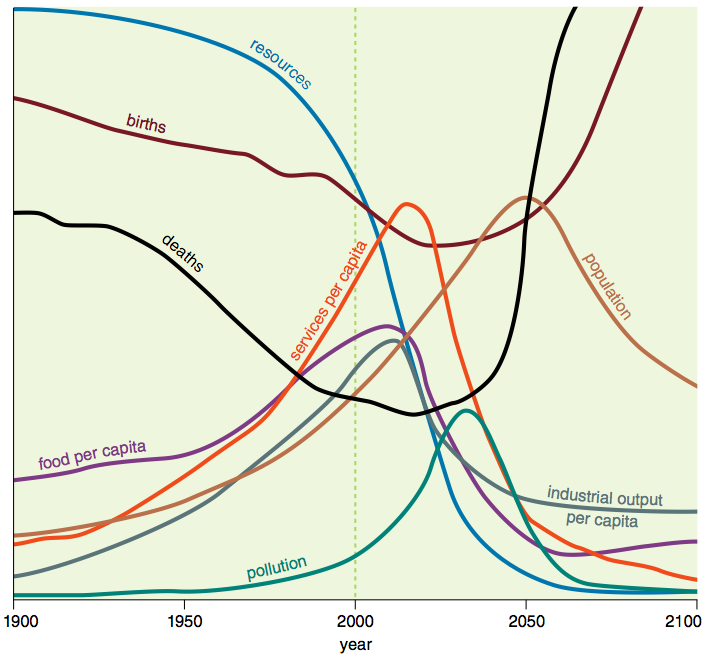

The only study to date modeling how long the economy can grow without seizing up is the one documented in the 1972 book The Limits to Growth, by D. Meadows et al. This analysis has proven to be surprisingly predictive. Several analyses, including this one by Charles Hall and John Day, have shown that the world economy is fairly close to “on track” with the base scenario shown in that book (Figure 1). If the world economy continues to follow this course shown, collapse would appear to be not more than 10 or 20 years away, as can be seen from Figure 1, below.

Figure 1. Base scenario from 1972 Limits to Growth, printed using today’s graphics by Charles Hall and John Day in “Revisiting Limits to Growth After Peak Oil”http://www.esf.edu/efb/hall/2009-05Hall0327.pdf

One of the findings of the 1972 Limits to Growth analysis is that lack of investment capital is expected to be a significant part of what brings the system down. (There are other issues as well, including excessive pollution and ultimately lack of food.) According to the book (p. 125):

The industrial capital stock grows to a level that requires an enormous input of resources. In the very process of that growth it depletes a large fraction of the resource reserves available. As resource prices rise and mines are depleted, more and more capital must be used for obtaining resources, leaving less to be invested for future growth. Finally investment cannot keep up with depreciation, and the industrial base collapses, taking with it the service and agricultural systems, which have become dependent on industrial inputs (such as fertilizers, pesticides, hospital laboratories, computers, and especially energy for mechanization).

Jorgen Randers’ 2052: A Global Forecast for the Next Forty Years

In 2012, the same organization that sponsored the original Limits to Growth study sponsored a new study, commemorating the 40th anniversary of the original report. A person might expect that the new study would follow similar or updated methodology to the 1972 report, but the approach is in fact quite different. (See my post, Why I Don’t Believe Randers’ Limits to Growth Forecast to 2052.)

The model in Jorgen Randers’ 2052: A Global Forecast for the Next Forty Yearsappears to be a Demand Based approach that perhaps uses a Hubbert Peak Model on the fossil fuel portion of the analysis. One telling detail is the fact that Randers mentions in the Acknowledgements Section only one person who worked on the model (apart from himself). There he thanks “My old friend Ulrich Goluke, for creating the quantitative foundation (statistical data, spreadsheets, and other models) for this forecast.” Ulrich Goluke’s biography suggests that he is able to prepare a Demand Model spreadsheet. It would be hard to believe that he that he could have substituted for the team of 17 researchers who put together the original Limits to Growth analysis.

The Need to Add to the Original Limits to Growth Analysis

The original Limits to Growth analysis was primarily concerned with quantities of items such as resources, pollution, population, and food. It did not get into financial aspects to any significant extent, except where flows of resources indicated a problem–namely in providing investment capital. One thing the model did not include at all was debt.

In the sections that follow, I show a model of how some parts of the economy that weren’t specifically modeled in the 1972 study work. If the economy works in the way described, it gives some insights as to why collapse may be ahead.

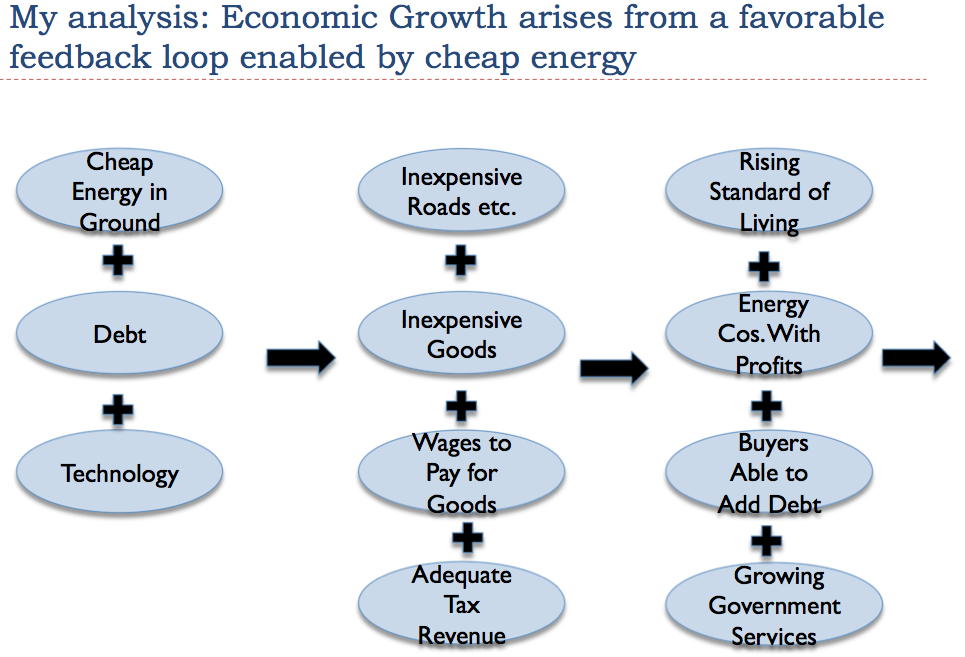

Economic Growth Arises from a Favorable Feedback Loop

Economic growth seems to arise from a favorable feedback loop, as shown in Figure 2, below.

Figure 2. Author’s representation of how economic growth occurs in today’s economy.

This model above is intended to reflect the situation from, say, 1800 to 2000. The situation was somewhat different before the use of fossil fuels, when far less economic growth took place. Furthermore, as we will see later in this post, the model changes again to reflect the impact of diminishing returns as the cost of energy production increases in recent years and in the future.

The critical variables that allow economic growth to take place are (1) cheap energy available from the ground, such as coal, oil, or natural gas–if cheap renewables were available, these would work as well (2) technology that allows us to put this cheap energy to work to make goods and services, and (3) a way to pay for the new goods and services.

Debt. In this model, debt plays a significant role. This happens because fossil fuels allow a huge “step up” in the quality of goods and services, and debt provides a way to bridge this gap. For example, with fossil fuels, we have electric light bulbs, metal machines in factories, and farm machinery, all of which vastly improve efficiency. The ability to pay for the new fuel and the new devices using the fuel, is much greater after the new devices using the fuel are put in place. The way around this problem is simple: debt.

The use of debt becomes important at many points in the economy. Increased debt can theoretically help (a) the companies doing the energy extraction, (b) the companies building factories to create the new goods and services, and (c) the end consumers, since all of these benefit greatly from the services that cheap fossil fuels provide, and can better pay afterward than before.

Government debt, such as debt used to finance World War II, can also be used to start and maintain the cycle. John Maynard Keynes noticed this phenomenon, and recommended using an increase in government debt to stimulate the economy, if it was not growing adequately. The detail he was unaware of is the fact that the debt only works in the context of cheap energy supplies being available to make use of this debt, enabling growth.

How the Feedback Loop Works. The loop starts with the combination of a cheap-to-exploit energy resource, technology that would use this resource, and debt that allows those would like to gain access to the resources to have the benefit of them, before they are actually able to pay cash for them.

This combination allows goods to be produced which initially may not be very cheap. Over time, new methods are tried, allowing technology to improve. Consumers are able to buy increasing amounts of goods and services, both because of their own increased productivity (enabled by fossil fuels and new technology) tends to raise their wages, and because the improving technology lowers the cost of goods. Government services are expanded as tax revenue per capita increases. Infrastructure such as roads are expanded making the economy more efficient.

In this context, profits of companies grow, allowing reinvestment. Investment is also enabled by increasing debt. This allows the cycle to start over again, with better technology and more infrastructure in place. The economy tends to grow, and the standard of living tends to rise.

Overview. One way of explaining the tendency toward economic growth is that a cheap-to-extract fossil rule has an extremely high return on investment. This very high return enables benefits to all: workers receive higher wages; businesses receive higher profits; and governments receive both higher tax revenue and the ability to build new roads and other infrastructure cheaply.

Another way of describing the tendency toward economic growth is to say that the value to society of the (cheap) energy product is far greater than its cost of extraction. This difference provides a benefit which flows through to many parts of the economy. Economists do not recognize that this situation can happen, but it seems to be a major source of economic growth.

The Spoiler: Diminishing Returns

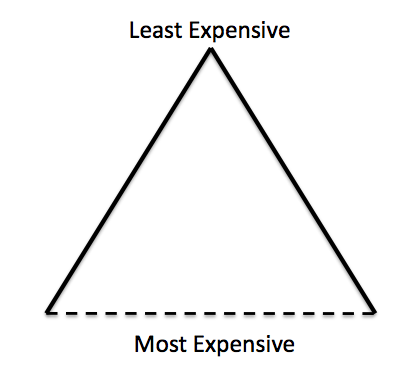

The problem with energy extraction is that we extract the inexpensive-to-extract energy sources first. Eventually these sources get depleted, and we need to move on to more expensive-to-extract energy sources. I illustrate this situation with a triangle that has a dotted line at the bottom.

Figure 3. Resource triangle, with dotted line indicating uncertain financial cut-off.

Businesses start by extracting the cheapest to extract resources, found at the top of the triangle. As these resources deplete, they move on to the more expensive to extract resources, further down in the triangle. Looking downward, it always looks like there are more resources available–it is just that they are more expensive to extract. This is why reported reserves tend to increase over time, even as supplies are depleted. The limit is a financial limit, illustrated by a dotted line, which is why virtually no one can figure out when the limit will actually arrive.

One somewhat minor point: When I say, “Cheapest to extract resources,” I am referring to broadly defined costs. What businesses want is resources that produce goods and services most cheaply for the consumer. Thus, they are really concerned about cheapest total cost, considering the entire chain that goes all the way to the consumer, including refining and transportation. The costs would include energy used in extraction, labor costs, transportation costs, taxes, and the cost of debt. It probably should include the cost of mitigating pollution effects as well.

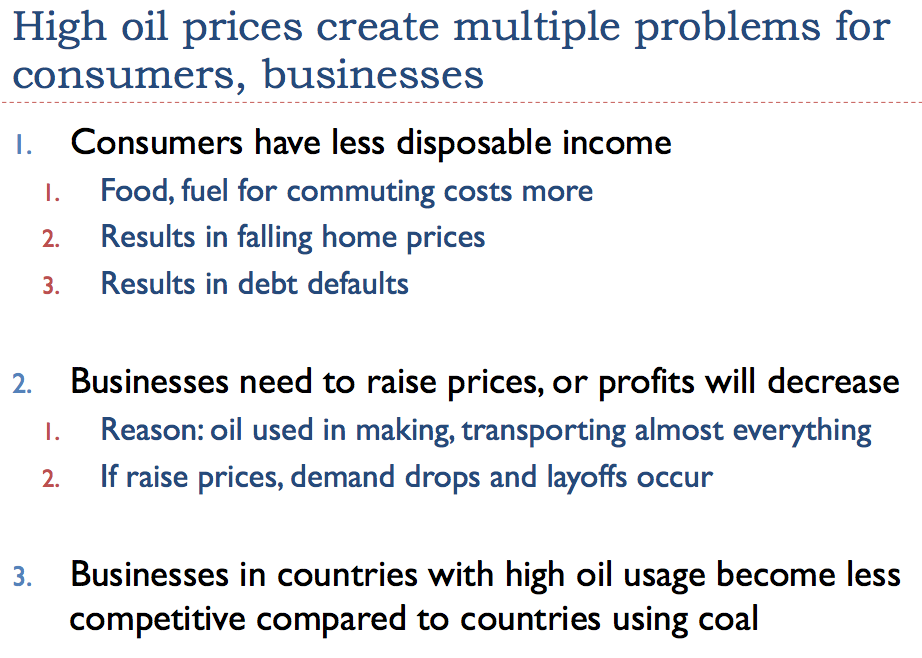

A major problem is that as the cost of energy extraction grows, the favorable gap between the cost of extraction and the benefit to society (as mentioned in the previous section) shrinks. There are many ways that this problem manifests itself in the economy. Figure 4 shows a list of such problem with respect to higher oil prices:

Figure 4. Image by author listing some of the problems created by rising oil prices.

One indirect impact of these issues is that there are more layoffs and fewer new job opportunities. If we calculate average wages by taking (total US wages) and dividing by (total US population), we see that during periods of high oil prices, wages tend not to grow, as they had in periods when oil prices were lower–just as we would expect (Figure 5, below).

Figure 5. Average US wages compared to oil price, both in 2012$. US Wages are from Bureau of Labor Statistics Table 2.1, adjusted to 2012 using CPI-Urban inflation. Oil prices are Brent equivalent in 2012$, from BP’s 2013 Statistical Review of World Energy.

Another issue is that it is not just the price of oil that rises. The price of natural gas rises as well. We have not felt this in the United States, because demand has kept the price down below the price of shale gas extraction. The cost of coal, delivered to its destination, has risen because transport uses oil, and transport costs are a significant share of total costs. The cost of base metals has also risen since 2002, because oil is used in metal extraction. Food prices in general have tended to rise as well, because oil is used in production and transport of food. When wages are close to flat, and the cost of many goods are rising, workers find that their paychecks are increasingly squeezed.

While costs of making goods in the US are rising, and paychecks are stagnating, an increasing amount of goods are imported from areas around the world where energy costs and wage costs are lower. This helps keep the cost of consumer goods down, but it makes the problem of lack of jobs for US workers worse.

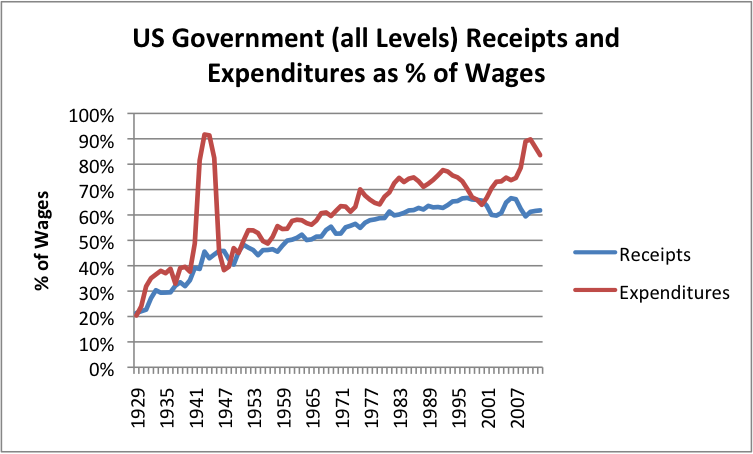

With all of these things happening, the government has more and more problems with its funding. Expenditures continue to rise, but taxes flatten, as the government tries to help the economy grow by not raising taxes to match expenditures (Figure 5, below).

Figure 6. Based on Table 2.1 and Table 3.1 of Bureau of Economic Analysis data. Government spending includes Federal, State, and Local programs.

Government expenditures can be thought of as expenditures out of the surpluses of the economy. As indicated previously, these are to a significant extent possible because of the favorable difference between the cost of extracting fossil fuels and the benefit those fossil fuels provide to the economy. As the use of fossil fuels has grown over the years, these government services have grown. In recent years, the presence of more unemployed workers has driven a need for more government services.

Since the early 2000s, government revenues have flattened. The lack of revenue, together with the ever-rising government spending, is what is driving continued big deficits. The danger is that this difference cannot be fixed, without huge cuts to programs that people are depending on, like unemployment insurance, Social Security and Medicare.

How the Economic Growth Loop Changes to Contraction

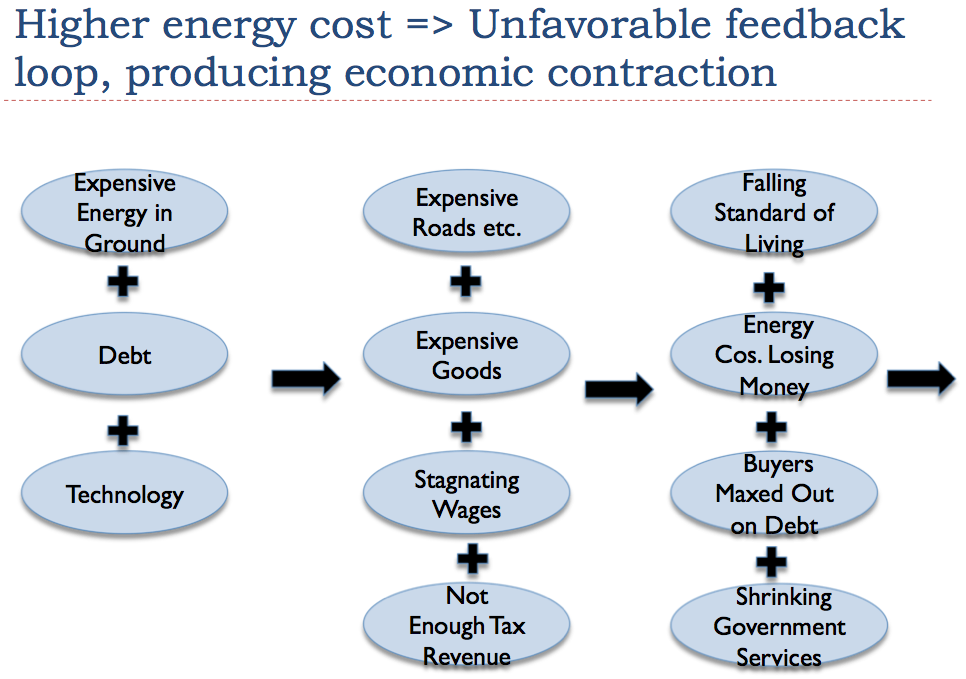

In my view, what causes a shift to contraction is a shift to higher energy costs. With higher energy costs, there is less surplus between the cost of extraction (broadly defined) and the benefit to society. Because of the smaller surplus, the parts of the economy that use this surplus, such as government spending, must shrink.

Figure 7. Higher energy cost leads to unfavorable feedback loop. (Illustration by author.)

We gradually find that all the great things we had learned to enjoy–inexpensive roads and other infrastructure, cheap goods, rising wages, and rising government serves–start going away. We increasingly find consumers maxed out on debt. We also find companies (especially energy companies) reporting lower profits, so they have more trouble investing in new energy extraction. The government cannot collect enough taxes for all of its services, so finds itself needing to keep raising its own debt levels.

The government can kind of “paper over” its difficulties with growing debt levels for a while, by using Quantitative Easing (QE). QE has the effect of making the interest the US must pay on its own debt lower. It makes the cost of business investment in new plants and equipment (including shale oil drilling) cheaper. It also helps stretch the incomes of increasingly impoverished workers by allowing monthly payments on homes and cars to be lower than they would otherwise would be.

The Party Ends With a Thud

Most readers can deduce that a shift from a growing economy to a shrinking economy is not a pleasant situation. It has all of the makings of collapse.

One of the big problems is debt defaults, as it becomes increasingly impossible to repay debt with interest. This creates conflict between borrowers and lenders. Debt defaults are also likely to cause huge problems for banks, insurance companies, and pension plans, because of the impact on their balance sheets. Some institutions may close.

To the extent new credit is cut off, the lack of credit cuts off new investment in energy extraction, in buying new cars and trucks, and in almost everything else. Such a cut-off in credit is likely to increase job layoffs and to lead to yet more defaults. Lack of investment in new energy extraction causes oil supply to fall quickly–far more quickly than standard “decline” models would suggest.

Businesses that in the past found that they could benefit from “economies of scale” as they grew find that fixed costs stay the same, even as sales shrink. This means that they either need to raise prices to cover their higher per-unit costs, or lose money.

Governments find that they need to cut government services to balance their budgets. Discontent grows among citizens as those who lose their benefits become very unhappy. Discord grows among political parties, because no one can agree how to cut programs equitably.

We don’t know how this will end, but we do know that the Former Soviet Union collapsed into its constituent parts when fossil fuel surpluses were reduced, prior to 1991. Egypt and Syria both have had civil unrest as their oil exports ended. Clearly very large government changes are possible, as surpluses disappear.

This list of potential impacts could be expanded endlessly, but I will spare readers from a more comprehensive list.