When I write about high oil prices having an adverse impact on the economy, quite a few readers respond by saying, “No, most (or all) of the problem is a debt bubble.” They seem to think that poor underwriting of mortgages a few years ago allowed a debt bubble. Once this bubble is past, or some similar bubble, our problems will be over.

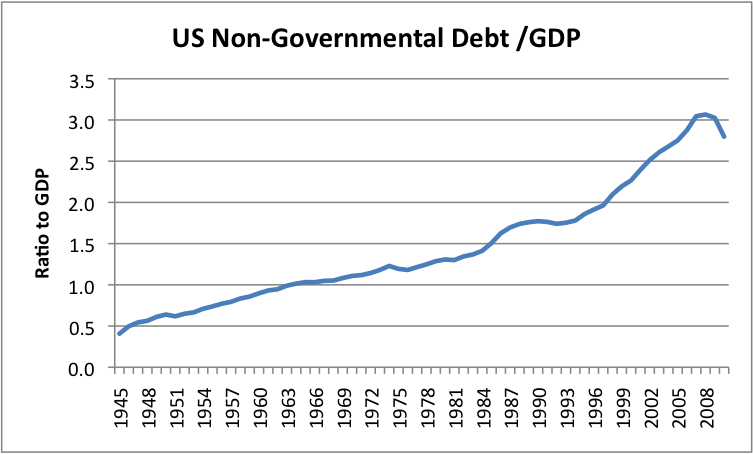

I decided to see when the debt bubble really started. The answer surprised me–it appears that we have been building a debt bubble since at least 1945 (Figure 1 – based on Federal Reserve data).

Figure 1. US Non-Governmental Debt, Divided by Nominal GDP

Furthermore, it appears that this 65-year bubble is beginning to deflate. I believe that this is occurring because high oil prices are putting a cap on economic growth. If I am right, it seems to me that the drop in non-governmental debt shown in Figure 1 can be expected expect to continue, possibly eventually dropping all the way back to the 1965 debt level–that is, about 15% of today’s debt level.

There is a close link between growing debt and growing GDP. GDP growth is a gross measure; it does not take into account the amount of debt required to finance this growth. The increasing level of debt since 1945 has enabled economic growth to be higher than it otherwise would be, and has allowed the US to buy goods and services from abroad that we could not otherwise afford. If high oil prices cause economic contraction, as I believe is the case, we may see the situation reverse itself. Instead of rising debt leading to growing GDP and growing imports, we may instead see shrinking debt leading to declining GDP and declining imports.

Such a situation would be bad from many perspectives–stock market prices, bond defaults, and ability to purchase needed goods from abroad. Commodity prices may drop as well, because many people are likely to be out of work.

Two Views of Debt

It seems to me that there are two basic views of debt:

Modern View. If the economy is expected to keep growing indefinitely, debt is viewed as helpful–something that will allow consumers to buy goods, and pay for them over the life of the goods and will allow businesses to build new facilities, and pay for them over the lives of the facilities. The existence of debt products also facilitates pension plans, since bonds are often used to fund pension plan. The Modern View also permits governments to offer “Social Security” plans to citizens, since the expectation is that the future will be at least as good as it is today.

Traditional View. If people believe that life is a roller coaster, with some good years, and some bad years, but no clear upward trend, then debt plays a more limited role. The expectation is that citizens will set aside funds in the good years, so that they will be able to take care of themselves in the bad years. If new businesses are formed, accumulated savings rather than debt will tend to be the major source of funding. Debt will still be used to a limited extent, for example, by governments to finance wars; by businesses to cover goods in transit; and by families who truly hit hard times. But citizens and businesses will generally be wary of debt, because of the frequency of debt defaults.

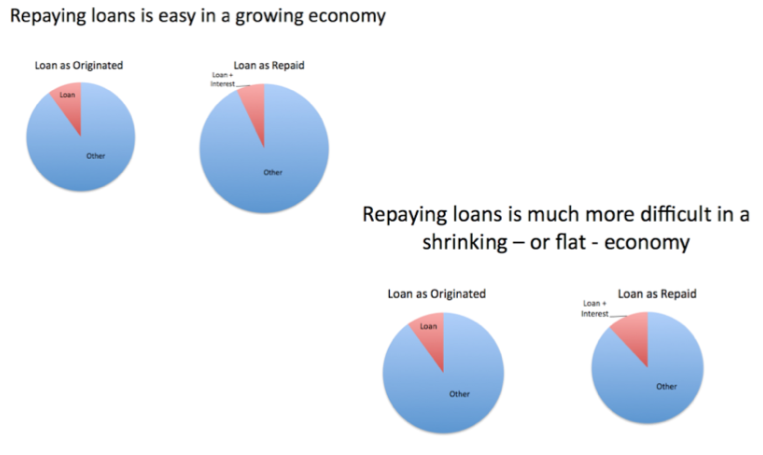

Admittedly, this summary is somewhat subjective, but it is tied to an observation I have made many times before: it is much easier to pay back debt with interest in times of economic growth than it is in times of economic contraction, as illustrated in Figure 2.

Figure 2. Repaying loans is easy in a growing economy, but much more difficult in a shrinking economy.

The Modern View of debt has gradually developed, as the world has expanded its use of fossil fuels, and as a result seemed to be on a never-ending growth path. Economists, actuaries, and financial planners have all built models assuming that growth will continue, and as a result, debt, and perhaps even growing debt, is possible. But back in 1945, many people in the United States still held the Traditional View of debt. Because of this, the level of debt was much lower than today, as illustrated in Figure 1.

What Happened after World War II

At the end of World War II, the US government found itself in the uncomfortable position of no longer needing as many workers, once the war effort was over. At the same time, it needed to repay the debt it used to finance the war. If no change were made in people’s spending habits, the result would have been a high unemployment rate (because of the layoffs) and a high tax rate (because of the need to repay the debt, with many unemployed).

Figure 3. US Governmental Debt (Including state and local debt) divided by nominal GDP, based on Federal Reserve and Bureau of Economic Analysis Data. Excludes internal governmental debt, such as Social Security Debt.

There was an obvious way to “fix” this problem: encourage citizens to borrow more. If people could be encouraged to borrow money to buy a new refrigerator or a new car or even a new home, then many more of these goods could be manufactured and sold. Businesses could also borrow to set up new manufacturing facilities. Little by little, what I have described as the Modern View of debt took over, and the ratio of non-governmental debt to GDP soared. GDP measures the cost of the new “stuff” sold, not whether the goods were bought on credit, so this approach greatly ramped up GDP.

Figure 4. Average annual increase in real GDP, for 10 year periods, based on Bureau of Economic Analysis data.

This approach of getting people to borrow more so as to ramp up economic growth worked very well in the early years, but less well recently, as can be seen from Figure 4. Part of the problem was that US oil supply started to decline in 1970, so that the US had to import more oil. The US also cut back on the kinds of goods it manufactured, with much of the heavy industry moving to other countries, necessitating more imports of such goods.

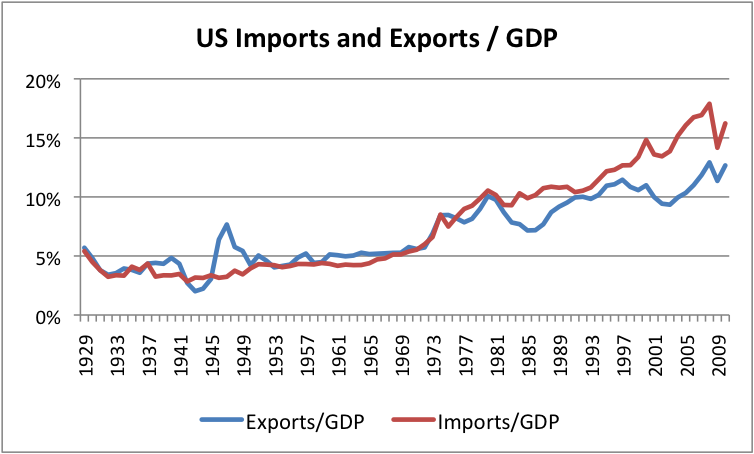

Figure 5. US imports and exports divided by GDP, based on BEA data.

The existence of all of the debt, and the fact that buyers in other countries would take government bonds in payment for goods and services, allowed Americans to continue to buy more goods and services imported from abroad, even though we did not have enough to trade in exchange.

A person might think our trading partners would have objected, but because US debt was considered a good investment, the system continued. For each year since 2001, the percentage growth in real GDP has been greater than the gap between exports and imports as a percentage of GDP–a hint that perhaps the situation was not really sustainable.

We saw in Figure 4, above, that over time, growth in real GDP decreased. At the same time, the amount of debt required to create each increment in GDP increased, as shown in Figure 6, below.

Figure 6. Increase in US Debt (all types including governmental) divided by increase GDP, for 10 year periods, based on Federal Reserve and BEA data.

Part of what happened was that a limit was being reached on how much debt reasonably could be carried. Almost everyone who could afford a house already had one. Businesses had expanded as much as they felt was prudent. Other kinds of debt that were added, but the new kinds of debt weren’t as efficient in providing funds to for citizens to actually buy things–securitization of mortgages, for example, and the interest rate “carry trade. ” In the early 2000s, some of the debt that was added was really ill-advised–allowing people with inadequate incomes to purchase homes, for example.

I don’t have figures for other parts of the world, but my impression is that many other countries followed a similar pattern of rising debt levels, as the Modern View of debt became the norm in economies around the world.

Where Do We Go From Here?

One popular view is that all we have to do is unwind some of the badly made loans, and the financial system can go on as before. Or perhaps we have raised the amount of debt too high, and the interest payments are now a drag on the economy. In this view, if we keep interest rates low, and bring the debt level down to that of a few years ago, maybe the economic system will work as before.

It seems to me that the real issue is that we live in a finite world. The idea that debt can continue to expand is simply false. The world economy will hit limits of many kinds–for example, the amount of low-cost oil that can be extracted; the amount of fresh water than can be obtained, without resorting to high-priced desalination; the amount of pollution that we can deal with, without huge health problems; the amount of CO2 that the atmosphere can absorb, without huge climate and ocean difficulties.

Because of these issues, the Modern View of debt is simply false. It is based on a temporary phenomenon. Debt can only expand for a while, in a finite world. Once we start hitting limits, debt expansion at first does less and less, and ultimately falls apart under its own weight.

It seems to me that the limit we hit first is that of adequate low-priced oil. There is plenty of oil theoretically available–but it is high-priced oil, that puts the economy into recession, as more resources need to be devoted to oil extraction, and fewer resources to other endeavors. Saudi Arabia and rest of OPEC claim the ability to provide more oil quickly, but when oil prices rise, they don’t really come through (Figure 7).

Figure 7. World and OPEC crude oil production, and Brent spot oil price, based on EIA data.

High-priced oil has caused financial difficulties for many governments around the world, because when oil prices rise, food prices tend to rise as well. Citizens cut back on discretionary goods when food and oil prices rise, causing recession. During recession, governments collect less taxes at the same time they are spending more on unemployment benefits and stimulus funds. As a result, governments are increasingly prone to debt defaults, such as those now being discussed for Greece and other European countries.

What I expect to see next is one country after another defaulting on its debt. Each default will set off a chain reaction of under-capitalized banks needing bail outs, and, as a result, more governments getting into financial difficulty. The IMF will try to fix the problems, but eventually the level of difficulty will be more than it can handle.

Where will the deleveraging stop?

This is the big question. More debt helps keep demand for goods and services up, and helps keep GDP growing. But the economy needs to be expanding, in order for it to make sense for debt levels to rise. If the economy is shrinking (or even flat), businesses don’t see a need to expand, so have no reason to borrow more money. Homeowners are worried about their jobs, so are not interested in buying more expensive homes. If high oil prices are part of the equation, higher prices for oil products and food cut back on the funds people have to pay for discretionary goods of all types.

It seems to me that there is a significant chance that we will find ourselves transitioning back from a Modern View of debt to a Traditional View of debt. If this happens, we are at risk of the ratio of debt to GDP dropping way back–not to 2005 levels, or 2000 levels, but to 1945 levels, or even lower. A big part of this slide downward might come through debt defaults. Such a change would greatly reduce this country’s ability to buy imported goods, and could result in huge economic dislocations.

I have not said much about governmental debt. The US Federal Government uses “cash-basis” accounting, rather than accrual accounting, so I don’t see its supposed debt level as being all that helpful in understanding its financial position. The US Federal Government’s liabilities are much higher than its stated debt level would suggest, since it makes many promises which it does not set up reserves to handle. For example, it guarantees bank deposits and pension plan payments, up to prescribed limits, but these guarantees are not reflected in its financial statements. The US government can theoretically issue more debt to meet its obligations, but there is no guarantee that Congress will continue to approve ever-rising debt levels, or that willing external buyers can be found for the debt.

I expect that the world will need to develop an entirely new financial system to fix the 65-year debt bubble. Our current debt-based approach simply is not workable without long-term growth. But making such a transition will very difficult–perhaps impossible. Individual countries can perhaps each set up their own system, but trying to integrate them would seem to be very difficult. It is possible that at some point we may find ourselves without an operating international financial system.

This is why I see the near-term outlook for the world financial system as very ominous. We have a seriously broken system, but no good way of fixing it.