This is a guest post from Erica Thompson, formerly with the UK Energy Research Centre (UKERC Report) and now working on a PhD at Imperial College, London. She attended the ITPOES report launch on our behalf.

– Chris Vernon, TOD editor

Today’s (10th Feb 2010) launch of the second report of the Industry Taskforce on Peak Oil and Energy Security (ITPOES) was rather more high-profile than the previous one. After summaries of the report from other contributors, Richard Branson arrived late to read out a short speech and media interest (informally measured by the rate of camera flashes) picked up; we can expect a scattering of news stories about the report to follow, in the usual places.

As we reach maximum oil extraction rates, the era of cheap oil is behind us. We must plan for a world in which oil prices are likely to be both higher and more volatile and where oil price shocks have the potential to destabilise economic, political and social activity.

Our message to government and businesses is clear. Act now.

Protagonists

Involved in the current report are:

- two construction companies: Arup and Foster + Partners

- two energy companies: Scottish and Southern Energy (one of the UK’s “Big Six” energy suppliers) and Solarcentury (group convener Jeremy Leggett’s solar energy installation firm)

- two companies with a stake in public transport: Stagecoach Group (the second largest transport firm in the UK) and Virgin (which has fingers in many pies but are here under a transport “hat”).

The above six firms all have a great interest in advocating action to reduce oil dependence, as they set out in the report and in their presentations at the launch. Government incentives or public infrastructure projects to improve energy efficiency, invest in renewable energy and increase use of public transport would benefit these companies directly. Of course, they also lay stress on the cost and risks to consumers, the need to reduce energy poverty, and in some cases a wish to contribute to reducing carbon emissions. Since the last report was published, FirstGroup (the largest transport firm in the UK) and Yahoo! have quietly absented themselves from the table. Whether or not other companies have been approached is unclear.

What’s new?

As before, they offer two “expert opinions” – one from Chris Skrebowski, with updates on the impact of recession and new shale gas developments, and one from economist Robert Falkner on economic consequences and the role of climate and energy policy. This reflects the shift in tone from the more technical first report to a greater emphasis on advocacy, remembering that a UK general election is imminent.

Economic modelling

Perhaps the most useful issues raised by the ITPOES report are the comments on risk to the UK’s balance of payments in the next decade:

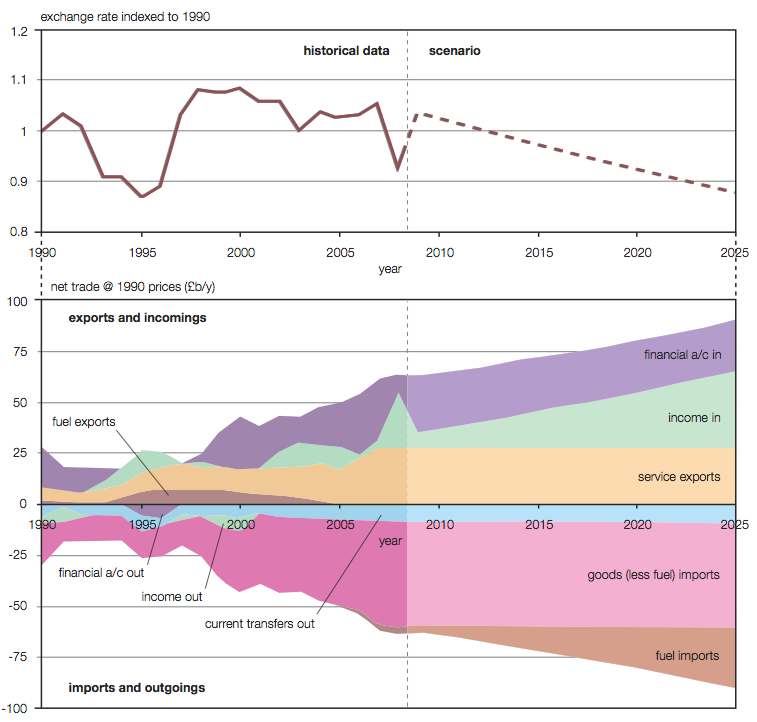

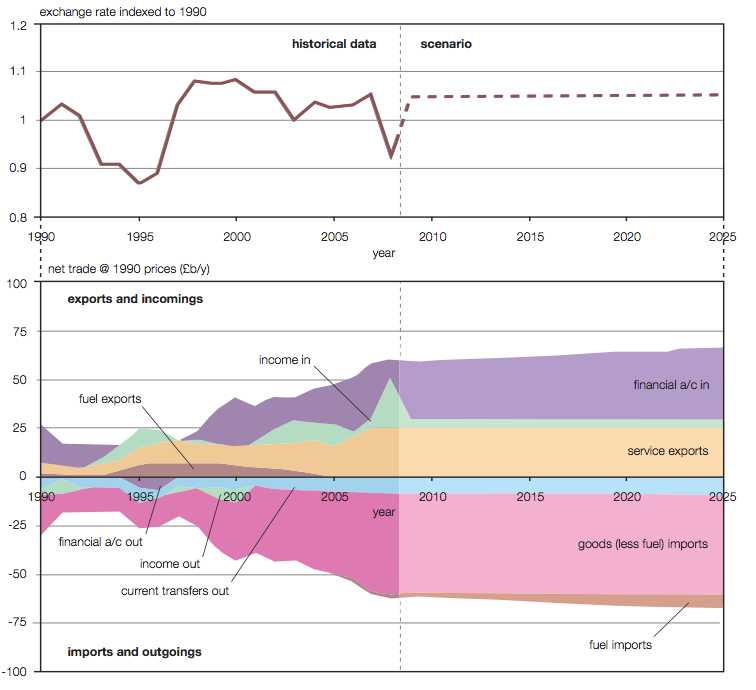

The UK, because it is now a net and rising importer of oil, gas and coal, is becoming increasingly exposed to competition for supplies from other energy importers. The insulation from international supply pressures provided when the UK was self- sufficient in oil and gas supply is now eroding quite quickly. This is likely to put pressure on the UK balance of payments and in a world of floating exchange rates is also likely to put downward pressure on the valuation of the pound sterling. In other words the positive benefits to the valuation of the pound as a petrocurrency are now disappearing.

Appendix D to the report considers this in more detail, with an (illustrative rather than predictive) model of the UK economy to 2025, developed by Arup. They consider two scenarios: one reactive (BAU) and one proactive. The proactive scenario assumes that some industrial output to consumer goods is diverted to investment in energy efficiency and renewables, and passenger car and freight oil consumption is reduced, so that total demand for fossil fuels is reduced to about 2/3 of the present level by 2025. The modelling is also interesting in being the first economic model I have seen which values both energy flows and capital stocks in energy units (petajoules and “virtual petajoules”). The result of a BAU reactive approach is “a continuous devaluation of sterling at an average of about 1 percent per year“.

Despite the somewhat simplistic modelling, there is a useful point here which is often unremarked; that the UK’s declining North Sea production threatens the balance of payments quite drastically in the next decade or so unless domestic energy demand can be reduced or, equivalently, domestic energy production increased. Even if, as in this analysis, the effects of volatility in oil prices and the possibility of supply shocks are neglected, there are clearly medium term structural problems with current UK energy policy which have further consequences for national energy security.

Recommendations

The recommendations of the report are divided into the categories of “general”, transport, retail and agricultural, power generation/distribution and heating policies. In most areas the recommendations are rather vague and and may be criticised by the cynical as self-serving (however, in what instance would we expect a company to make any other recommendations?). Actual reductions in service demand are skirted around carefully. Conspicuous by its absence is any mention of a carbon price, which was only mentioned in passing by Brian Souter (of Stagecoach, and clearly the most environmentally motivated of the group) at the launch.

Government response

A recurring theme of the morning’s speakers was the need to move “from recognition to action”. This was echoed by a representative of the UK Department for Energy and Climate Change (DECC) in an official response to the report, emphasising their own commitment to move “from strategy to delivery”. The response was muted in tone, sticking to the party line that DECC “are already taking action” and citing a list of their projects from last summer’s Low Carbon Transition Plan – which did not mention oil depletion, even obliquely. It seems that peak oil, though evidently recognised within DECC, remains somewhat unutterable as a specific motive for action. Whether or not it still influences policy decisions remains to be seen.

Conclusions

Although there is little new analysis, this report marks a further milestone as energy security issues continue an inexorable rise up the national agenda. Coming on the heels of a new consultation by the energy regulator Ofgem on energy security and longer term energy policy, and in the run-up to a general election, the report is what it set out to be: a well-timed wake-up call to British industry and government. Whether it will be heeded remains to be seen. Criticism is likely to focus on the (unavoidable) specific motivations of the partner companies, the (perhaps necessarily) simplistic approach to analysis and the (very much contestable) implicit assumptions. Nevertheless, the high profile of the companies and individuals involved is a marker of the increasingly widespread, if overdue, recognition of the UK energy dilemma, and the fact that DECC were represented at the launch event of a report with Peak Oil in the title is certainly a step in the right direction.

The first report (2008) was discussed on The Oil Drum here:

UK Industry Taskforce Sounds Alarm on Peak Oil

And Leggett provided further comment here:

Jeremy Leggett discusses the UK Industry Taskforce on Peak Oil and Energy Security